If your summer cash is sitting idle, you may be giving up easy returns. Before you fund a trip, buy a Father’s Day gift, or prep for Prime Day, it pays to compare where that money waits.

| Option | Best Timeline | Protection/Access | Main Strength | Main Drawback |

|---|---|---|---|---|

| U.S. HYSA | 2 weeks to 6 months | FDIC/NCUA; easy transfers | Simple and predictable | Rate may be slightly lower |

| Korea Investment & Securities cash-style account | 1 to 6 months | Depends on product; brokerage app access | Convenient for existing investors | More complexity and tax questions |

| NH Investment & Securities cash-style account | 1 to 6 months | Depends on product; brokerage workflow | Useful inside one investing platform | Settlement and product structure vary |

| Checking account | Immediate spending | Fastest access | No setup needed | Very low yield |

01 The short version before you move a single dollar

Ever set aside $600 for a July beach trip, then watch it sit in a checking account earning almost nothing? That mistake gets expensive fast. For short-term goals like Father’s Day gifts, Prime Day shopping, or an August vacation, the best home for cash usually comes down to two lanes: a U.S. high-yield savings account or a Korean brokerage cash-style product.

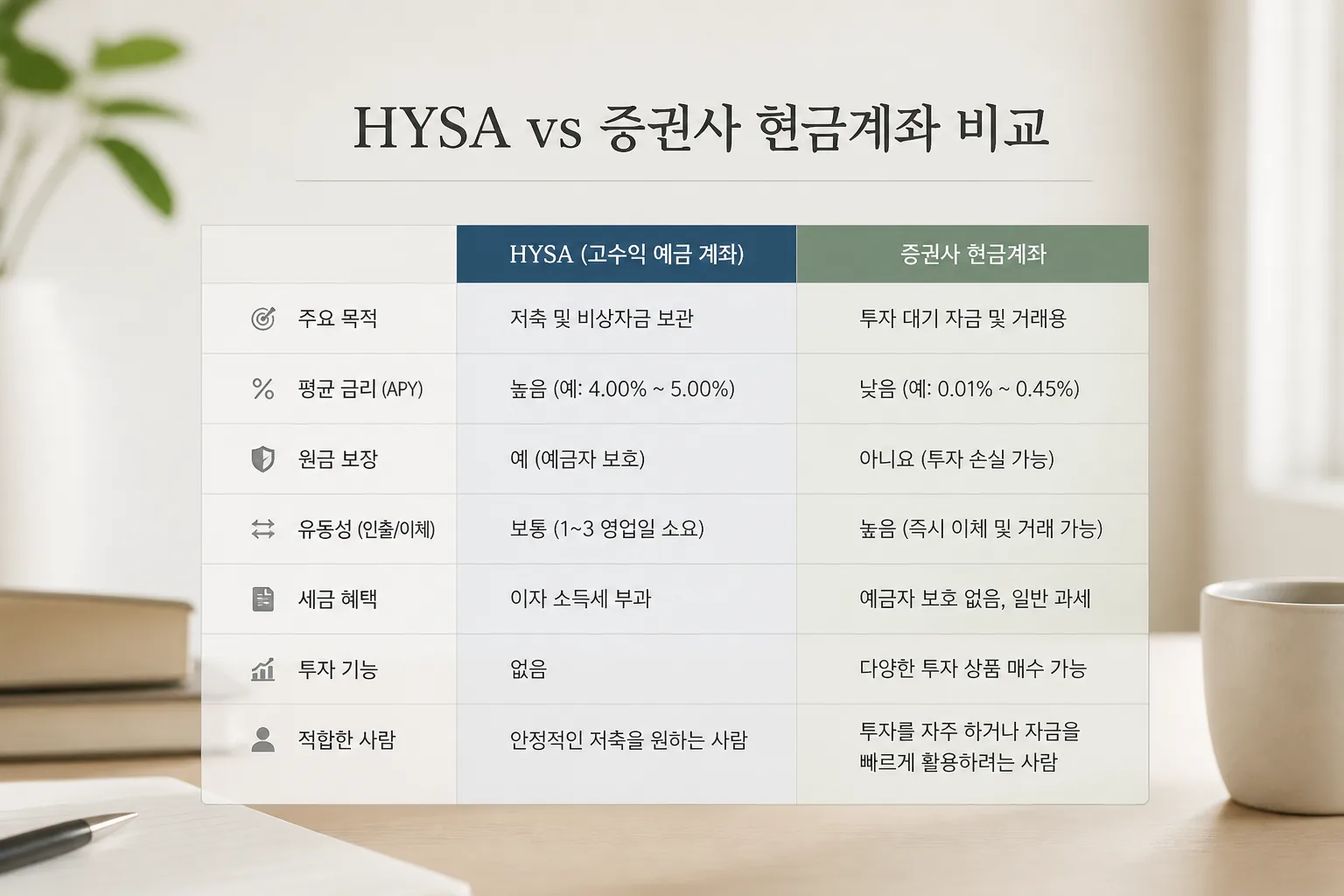

A plain HYSA wins on simplicity, FDIC or NCUA protection, and fast access. A brokerage cash option at firms like Korea Investment & Securities or NH Investment & Securities can offer competitive yields or linked products, but the trade-off is extra tax paperwork, settlement timing, and product complexity. I’ve seen friends overcomplicate a 3-month savings goal chasing a tiny yield edge. For $500 to $3,000 goals, convenience matters more than bragging rights.

read our guide to choosing a savings account

If you need the money in 7 to 45 days, access speed matters almost as much as rate.

Next, let’s sort out where each option actually shines.

02 Where HYSAs quietly beat brokerage cash

A good HYSA is boring in the best way. In June 2026, many readers will be comparing APYs, but the real filter is timeline. If you’re saving for a Father’s Day gift in 2 weeks or Prime Day in 1 month, a HYSA usually gives you same-bank transfers, predictable interest, and no need to think about market-hour cutoffs.

Here’s the practical checklist:

- Best for: 2 weeks to 6 months

- Typical priority: liquidity, deposit insurance, no trading setup

- Watch for: withdrawal limits, transfer holds, teaser rates

That interest won’t fund the whole vacation, obviously. But it keeps your trip money separate and harder to raid for takeout on a Thursday night. That alone helps.

The Korean brokerage side gets interesting once yield hunters start looking past convenience.

03 What Korean brokerage cash products get right — and where they get messy

At 한국투자증권 and NH투자증권, cash management can mean a sweep-style balance, a CMA-type account, or linked short-term products. That can be useful if you already invest there and keep idle cash in one ecosystem. A Seoul-based reader funding a 500,000 won summer budget may like that setup more than opening a fresh bank account just for one season.

But here’s the catch. Brokerage cash is not always the same as insured bank savings, and product details can change by account type, underlying instrument, and tax treatment. Korean investors may also compare linked dividend products or promotional savings plans, yet those are often built for a different goal than a 30-day shopping fund.

A slightly higher yield loses its appeal when access takes two extra steps.

- Best for: existing brokerage users, parked cash, slightly longer timelines

- Less ideal for: gift money needed this week, first-time savers, cross-border confusion

- Check first: settlement timing, fees, tax withholding, app usability

see our beginner guide to cash management accounts

Quick recap: if your goal is fixed and near, friction is the enemy. That leads straight to the side-by-side view most readers actually need.

04 A simple side-by-side for summer travel, gifts, and Prime Day

Below is the comparison I’d use for a real household budget, not a spreadsheet fantasy.

For short-term savings, the winner is usually the account you won’t hesitate to use.

05 Pick the account by deadline, not by hype

If your purchase date is locked — June 15 for Father’s Day, mid-July for Prime Day, August 1 for airfare — keep it simple. Use a HYSA for short, fixed goals. Use a brokerage cash option only if you already know the platform, understand the tax angle, and won’t need instant access.

Here’s what to do today:

- Put each goal on a calendar with the exact spending date.

- Keep any money needed in under 45 days in the easiest-access account.

- Compare net yield after taxes, transfer delays, and headaches.

related: how to build a summer travel budget

That’s the real play: match the tool to the deadline, keep the money visible, and don’t let a tiny rate gap derail a very real plan.