Trying to save for a trip, buy a Father’s Day gift, and still invest without overthinking it? The ETF vs index fund choice gets a lot clearer once dividends and timing enter the picture.

| Option | Best Use | Trading Style | Main Strength | Main Risk |

|---|---|---|---|---|

| Broad Index Fund | Monthly saving for long-term goals | Once daily at NAV | Simple automation | Less control over entry price |

| Broad Market ETF | Flexible investing with live pricing | Intraday trading | Tactical entries | Timing mistakes |

| Dividend ETF | Income-focused gifting or long-term holding | Intraday trading | Cash distributions | Yield chasing and sector concentration |

01 A June trip, a Father’s Day gift, and one investing choice

Ever tried saving for a summer vacation while hunting for a smart Father’s Day gift? That’s where a lot of beginners land in June 2026: one goal is 3 months away, the other feels emotional, and Prime Day ads are yelling from every screen.

The short version: index funds fit steady autopilot investing, while ETFs give you live pricing and tighter control during market hours. If you’re using 한국투자증권 or NH투자증권, that difference matters on day 1, not just years later. I’ve seen new investors focus on one shiny word — 배당, or dividend — and miss the stuff that actually moves results: fees, taxes, and whether the payout can hold up through a rough quarter.

read our beginner investing guide before your first order

A high yield can look like a gift. Sometimes it’s just a warning label.

If your June 2026 plan includes airfare, hotel costs, and maybe a small investment gift for Dad, the next decision is less glamorous but far more important.

02 What changes when you pick an index fund instead of an ETF

Here’s the plain-English version. Index funds are usually bought once per day at the fund’s closing net asset value. ETFs trade like stocks, so prices move all session long. That sounds minor. It isn’t.

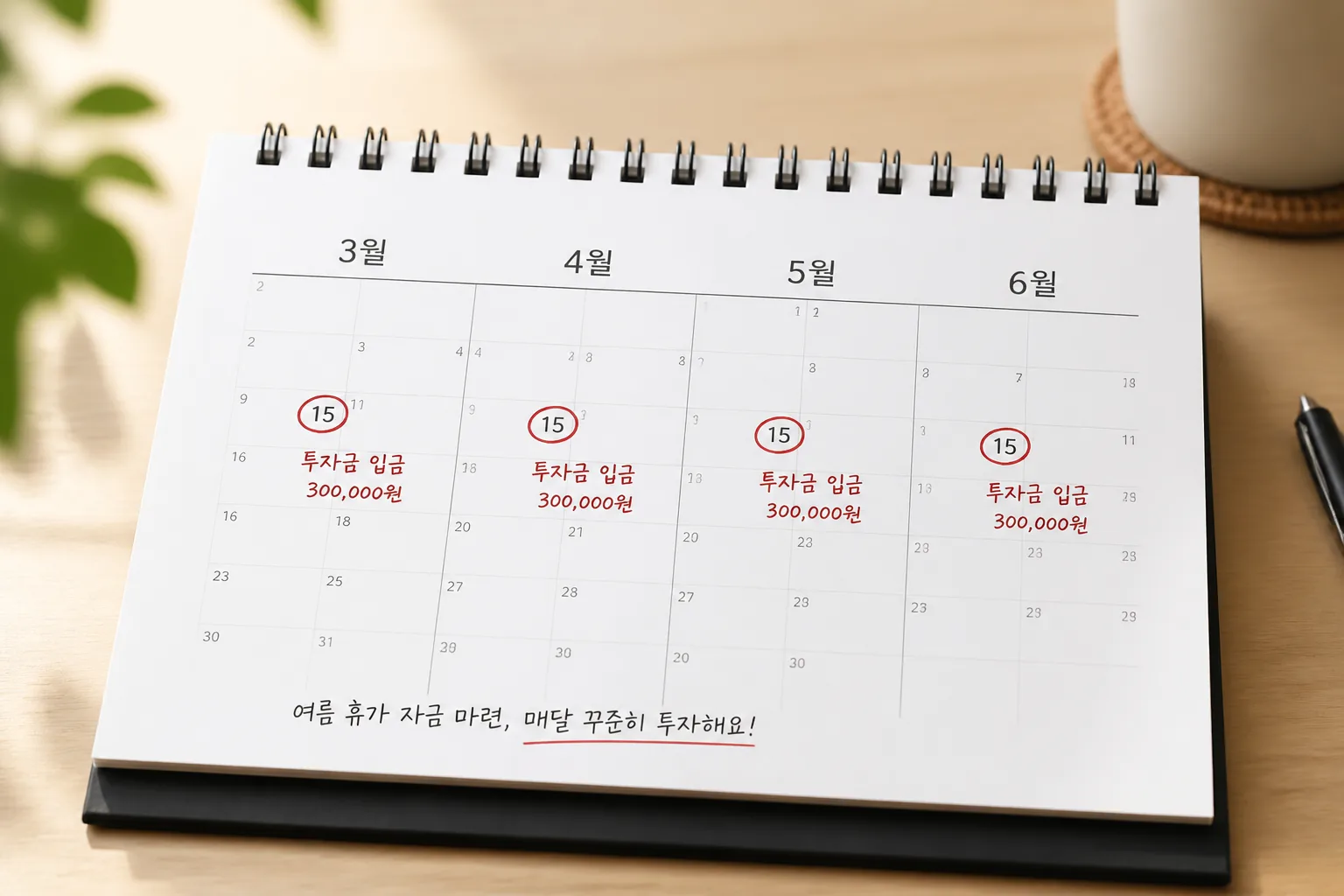

Say you want to set aside KRW 300,000 every month from March to June 2026 for a summer travel fund. An index fund works well because the habit matters more than the minute-by-minute price. It’s like using an automatic transfer for rent. Boring, yes. Effective too.

An ETF feels better if you want flexibility before a market event, a U.S. CPI release, or a Prime Day-driven retail rally in early July. A friend of mine did exactly this in 2024 with a dividend ETF and learned a painful lesson: he bought for the yield, ignored the expense ratio, and gave back part of the payout in costs.

Quick recap:

- Index fund: simpler, cleaner, easier for monthly automation

- ETF: tradable intraday, often lower minimums, more tactical

- Both can track the same benchmark, but the experience is different

The real question isn’t which one is better in theory. It’s which one matches your deadline.

03 The dividend trap beginners walk into every June

Dividend-focused investing sounds perfect for Father’s Day, right? Buy something that pays cash, call it a thoughtful long-term gift, and feel responsible. I get the appeal. Honestly, it’s a good instinct — just not enough on its own.

A 6% yield can beat a 3% yield on paper, but that headline number says nothing about payout stability, sector concentration, or tax treatment. Some high-yield products lean heavily on banks, energy, or REITs. One bad cycle and the income story gets shaky fast. Yield without context is how beginners get burned.

Look at 3 checks before buying:

- Expense ratio: a low-cost fund keeps more of each payout working for you.

- Distribution history: one strong quarter means little; 3 to 5 years tells a better story.

- Underlying index: broad-market dividend exposure usually behaves differently from a narrow, high-yield screen.

Next up is the platform angle, because even a decent fund can feel confusing inside the wrong brokerage app.

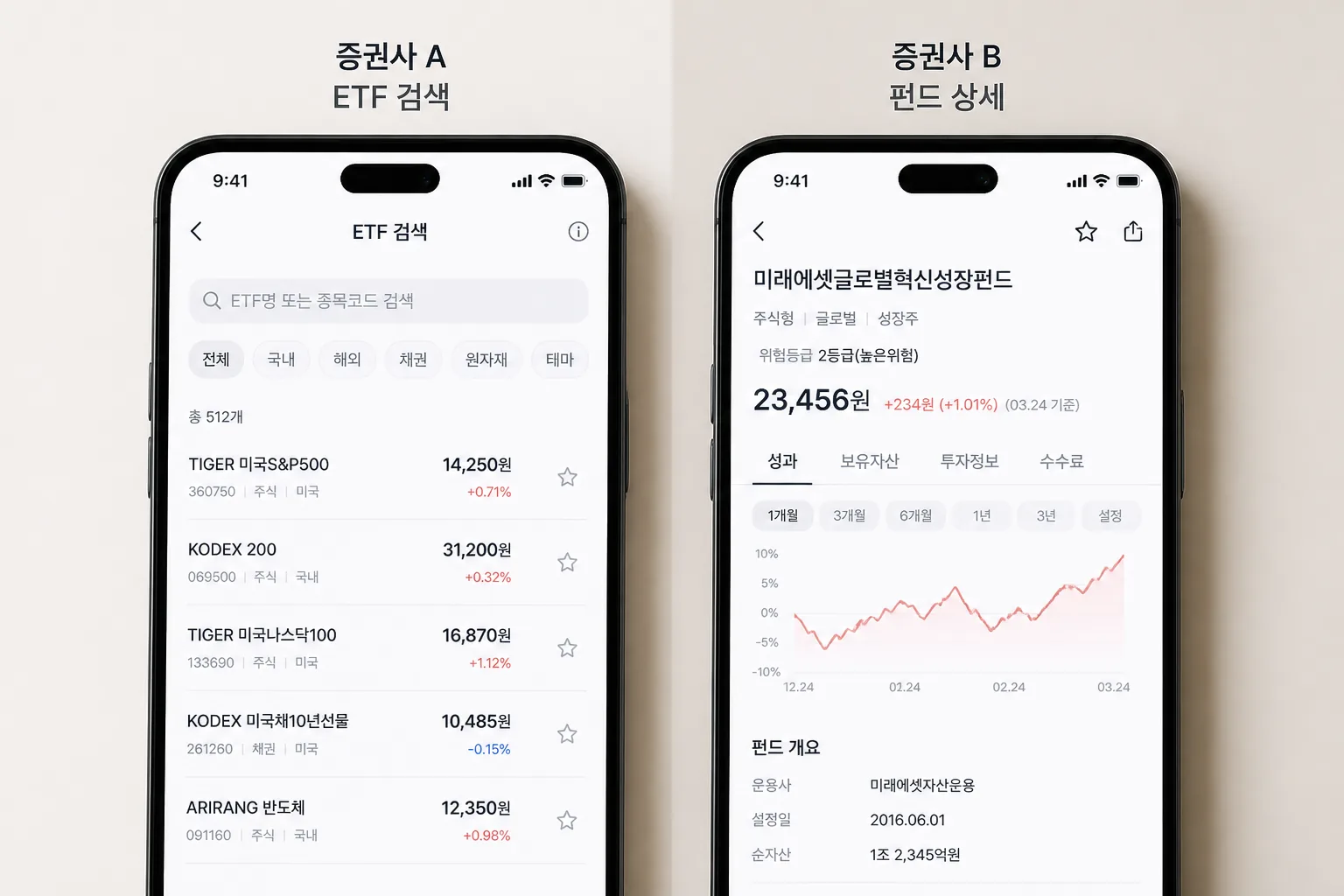

04 Using 한국투자증권 or NH투자증권 without making it harder than it is

Both 한국투자증권 and NH투자증권 give beginners access to domestic products, research tools, and mobile trading. What matters first is not the logo. What matters is order flow, fee visibility, and whether automatic investing feels easy at 8 p.m. on a Tuesday.

When I test brokerage apps, I look for 4 things in under 10 minutes: account setup friction, ETF search quality, fund detail depth, and whether recurring purchases are obvious or buried. If you plan to invest KRW 100,000 to KRW 500,000 per month, ease beats fancy features every single time.

- Choose an index fund if you want a set-and-forget June 2026 savings habit.

- Choose an ETF if you want live execution and easier tactical entries.

- Choose a dividend tilt only if you understand the payout schedule and risk.

see our guide to choosing a beginner brokerage account

related: dividend investing basics for first-time buyers

The best platform for a beginner is the one that makes the second purchase easy, not the first one exciting.

That leaves one final piece: what to do today, before June gets away from you.

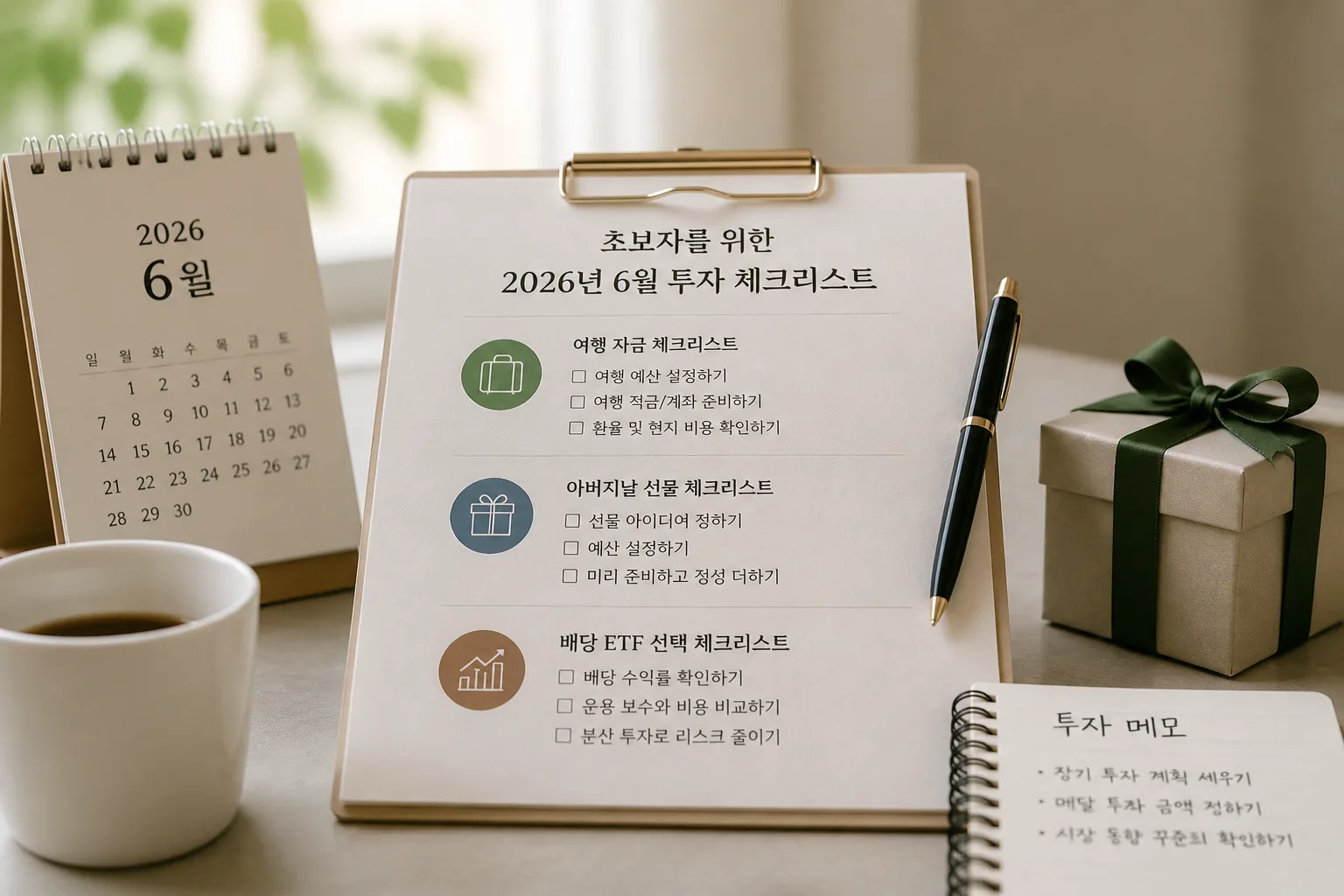

05 3 smart picks for June 2026 — and the move to make today

If you want a practical framework, here it is. Pick one lane, fund it, and ignore the noise for 30 days. That alone puts you ahead of most first-time investors.

3 smart picks by goal:

- Vacation money needed by June or July 2026: keep most of it in cash or a cash-like vehicle, not a dividend ETF.

- Father’s Day gift with a long horizon: a broad, low-cost index fund or broad dividend ETF makes more sense.

- Small tactical position before Prime Day: use an ETF only if you’re comfortable with price swings during market hours.

Do these 3 things today:

- Open 한국투자증권 or NH투자증권 and shortlist 2 broad index products and 2 dividend products.

- Write your timeline beside each goal: 30 days, 6 months, or 5 years.

- Buy only the product that matches the timeline.

read our travel budgeting guide before booking summer flights

That’s the real edge here. Not chasing the highest yield, not timing every dip — just matching the tool to the job. Period.