Trying to fund summer travel, a Father’s Day gift, and Prime Day deals at the same time? A small APY difference could leave more room in your budget than you expect.

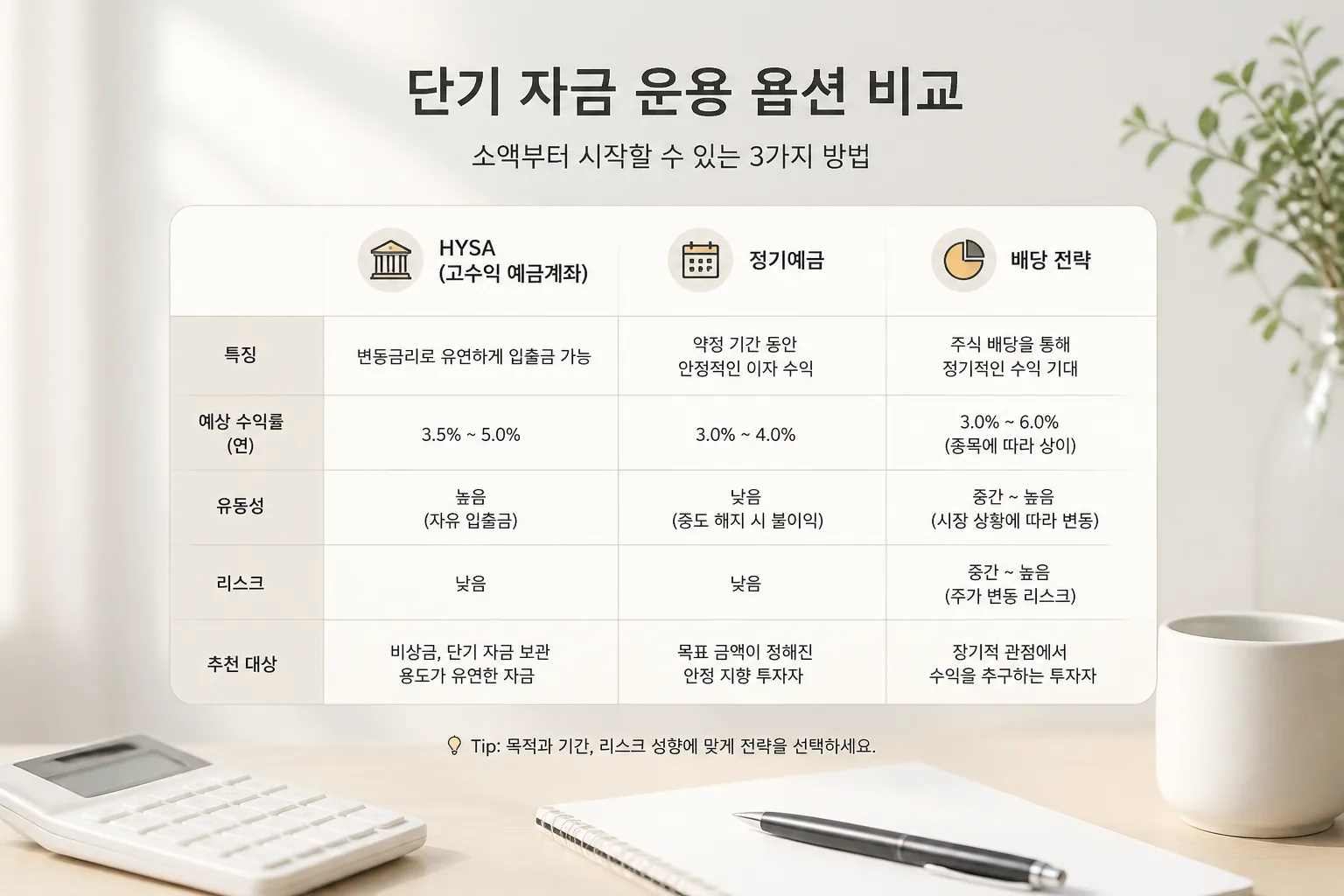

| Option | Typical Yield/Return | Access Speed | Best Use | Main Risk |

|---|---|---|---|---|

| HYSA | Around 4% to 5% APY | Usually 1-3 business days | Vacation, gifts, sale prep | Rate can change |

| 적금 | Often fixed promotional rate | Locked until maturity | Forced saving for known dates | Penalty or lower return if broken early |

| Dividend ETF/Stock | Yield varies, often 2% to 5%+ | Sell anytime market is open | Goals 12+ months away | Price volatility |

01 The $5,000 question before summer starts

Ever move $5,000 into the wrong account in June and realize 30 days later you boxed yourself in? That mistake hits harder when the money was meant for a July beach rental, a $150 Father’s Day gift, and Prime Day deals two weeks later.

Here’s the short version: for short-term goals, a high-yield savings account usually makes the most sense. You keep liquidity, FDIC or NCUA coverage usually applies within limits, and you’re not forced to wait out a term or stomach stock-price swings. That matters if your airline fare jumps on June 18 or your kid says Dad wants a new grill, not a tie.

build an emergency fund without overthinking it

When I’ve tested short-term savings setups myself, the friction tells the story fast. A HYSA lets you park cash today and pull it back in a day or two at many banks. A fixed-term 적금 rewards discipline, sure, but early-withdrawal rules can wreck the plan. Dividend investing can pay more over time, yet time is the catch. You may need the cash in 21 days, not 21 months.

For money you’ll spend this summer, flexibility usually beats chasing the last extra dollar.

Next, let’s look at the actual math, because the gap is smaller than most people expect.

02 What the math says in June 2026

Say you stash $5,000 in early June 2026. If a HYSA pays 4.50% APY, one month of interest is roughly $18 to $19 before tax. If a bank 적금 offers 4.80% but locks the money for 6 or 12 months, your edge over the HYSA for that first month is tiny. Really tiny.

Here’s a clean comparison:

| Option | Typical June 2026 use | Upside | Tradeoff |

|---|---|---|---|

| HYSA | Vacation, gifts, Prime Day | Fast access, insured cash | Rate can change |

| 적금 | Forced saving for a set date | Predictable return | Early withdrawal pain |

| Dividend ETF/stock | Longer goals, 12+ months | Income plus upside | Price drops can erase gains |

A friend of mine used a 12-month savings product for a September trip, then had to break it in July for car repairs. The rate looked great on paper. The real return after penalties? Pretty underwhelming, honestly.

That leads to the part banks rarely advertise: the hidden cost of being locked in.

03 What nobody tells you about access speed

APY gets the headline. Access rules decide the winner. That’s the part people miss.

For a summer fund, you may need three withdrawals in one month: $900 for flights, $150 for Father’s Day, $400 for Prime Day. A HYSA usually handles that rhythm better than 적금, which is built more like a commitment device. That structure helps chronic overspenders, no question. But if your timeline is messy, life wins.

Dividend strategies are even trickier. Yes, some blue-chip names and dividend ETFs throw off cash. But a 3.5% yield doesn’t protect you if the share price drops 6% before checkout day. Ask anyone who bought income stocks for a short goal in a choppy market. I’ve seen that movie before, and the ending is rarely fun.

Short-term savings is less about maximizing return and more about avoiding bad timing.

Quick recap:

- HYSA: best for flexibility

- 적금: best for forced discipline

- Dividends: best for longer horizons

There’s still one exception worth talking through, because not every saver needs pure flexibility.

04 Who should pick each option this month

Pick a HYSA if your spending date is uncertain, your target is under 6 months, or you want one place for vacation, gifts, and sale shopping. That’s the cleanest fit for most households in June.

Pick 적금 if you know you’ll sabotage yourself. I mean that kindly. If automatic monthly deposits of $300 keep your hands off the money until December, the structure can be worth more than a slightly better rate elsewhere. Behavior beats theory all the time.

Pick a dividend strategy only if the summer goal is optional and your real horizon is closer to 2027. That changes the whole decision.

see our guide to investing basics before buying dividend funds

CD vs savings account for short-term cash goals

The best move now is pretty simple, and you can do it before dinner.

05 Your next 20 minutes, mapped out

If you’re saving for summer 2026, don’t over-engineer this. Open a HYSA for the core fund, then split the balance into named buckets if the bank offers that feature. Put the trip money, the Father’s Day budget, and Prime Day cash in separate labels. Clean. Visible. Harder to raid.

Do these 3 things today:

- Compare 3 HYSAs and write down the APY, transfer speed, and minimum balance.

- Set one automatic transfer for every payday, even if it’s just $75.

- Keep dividend investing separate unless the goal is at least 12 months away.

If your target is short and specific, liquidity is part of the return. That’s the line to remember. Chase a little yield if you want, but don’t trap June money in a product built for December. That’s how a smart savings plan turns annoying fast.