If you’ve ever stared at two rewards cards and still had no clue which one was better, you’re not alone. The fine print changes everything.

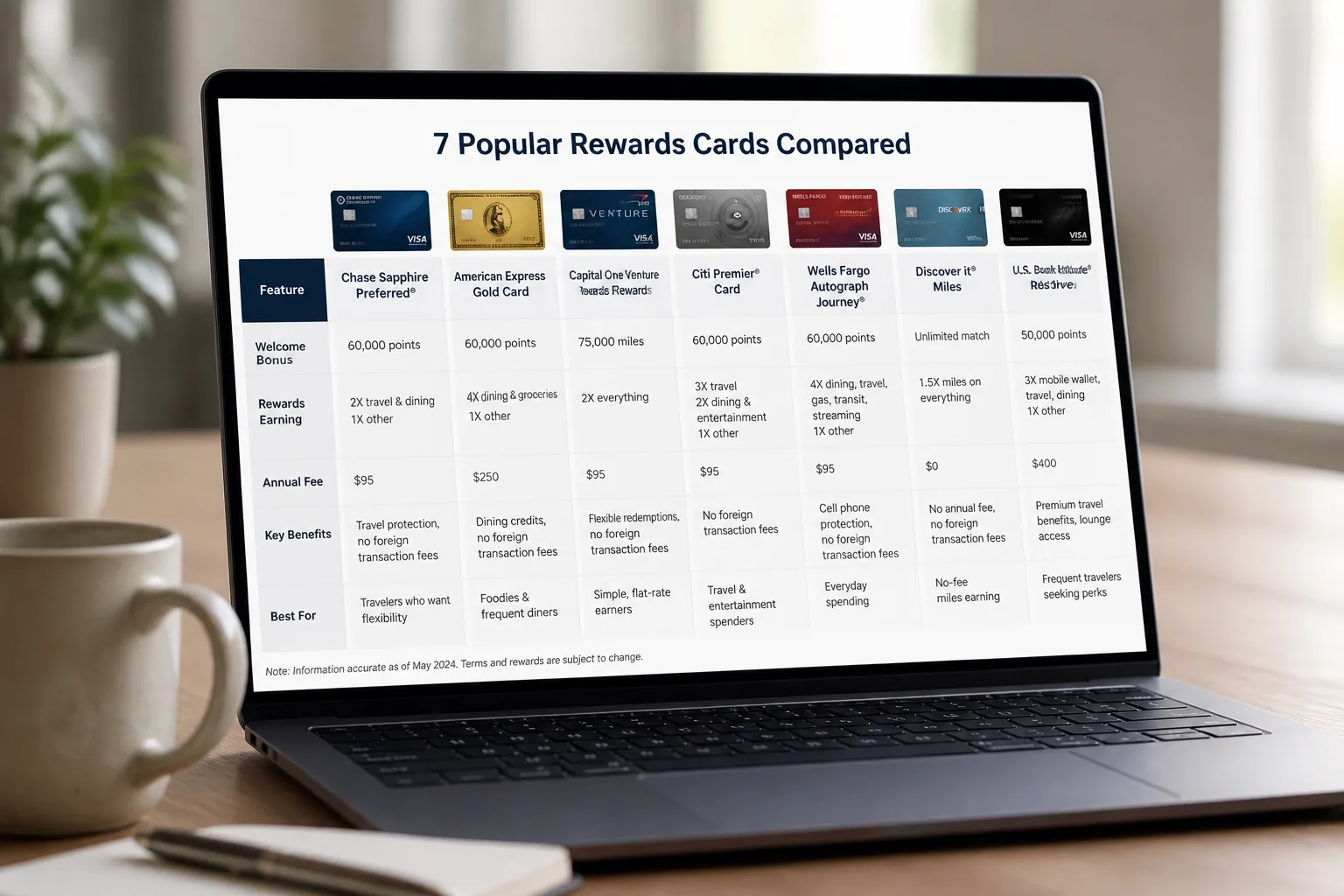

| Card | Annual Fee | Rewards Rate | Best Fit |

|---|---|---|---|

| Citi Double Cash | $0 | 2% cash back | Simple everyday spending |

| Wells Fargo Active Cash | $0 | 2% cash rewards | No-fee flat-rate users |

| Blue Cash Preferred | $95 | 6% groceries, 3% gas | Families with supermarket spend |

| Chase Sapphire Preferred | $95 | Travel and dining points | Travelers who want flexibility |

| Capital One Venture | $95 | 2x miles | People who want simple travel rewards |

| Amex Gold | $250 | 4x dining, 4x groceries | Heavy dining and food spending |

| Co-branded airline or hotel card | $0-$150 | Brand-specific points | Loyal airline or hotel users |

01 The headline bonus is rarely the real prize

Ever notice how every rewards card looks amazing for about 30 seconds? Then the annual fee, spending cap, and redemption rules show up, and the math gets messy fast.

Here’s the short version: a smart credit card rewards comparison starts with your spending, not the issuer’s marketing. A family spending $900 a month on groceries needs a different card than a consultant booking two flights a month. I’ve done this exercise with my own wallet before, and honestly, the biggest surprise was how often a boring 2% cash-back card beat a flashy travel card after year one.

Read more about picking the right credit card

The best rewards card is the one you’ll actually use correctly for 12 straight months.

That’s why the seven-card field below matters less than the categories behind it: flat-rate cash back, bonus-category cash back, airline or hotel cards, and flexible points. Once you sort cards that way, the fine print gets a lot easier to spot.

02 7 cards, 4 lanes, and one simple way to compare them

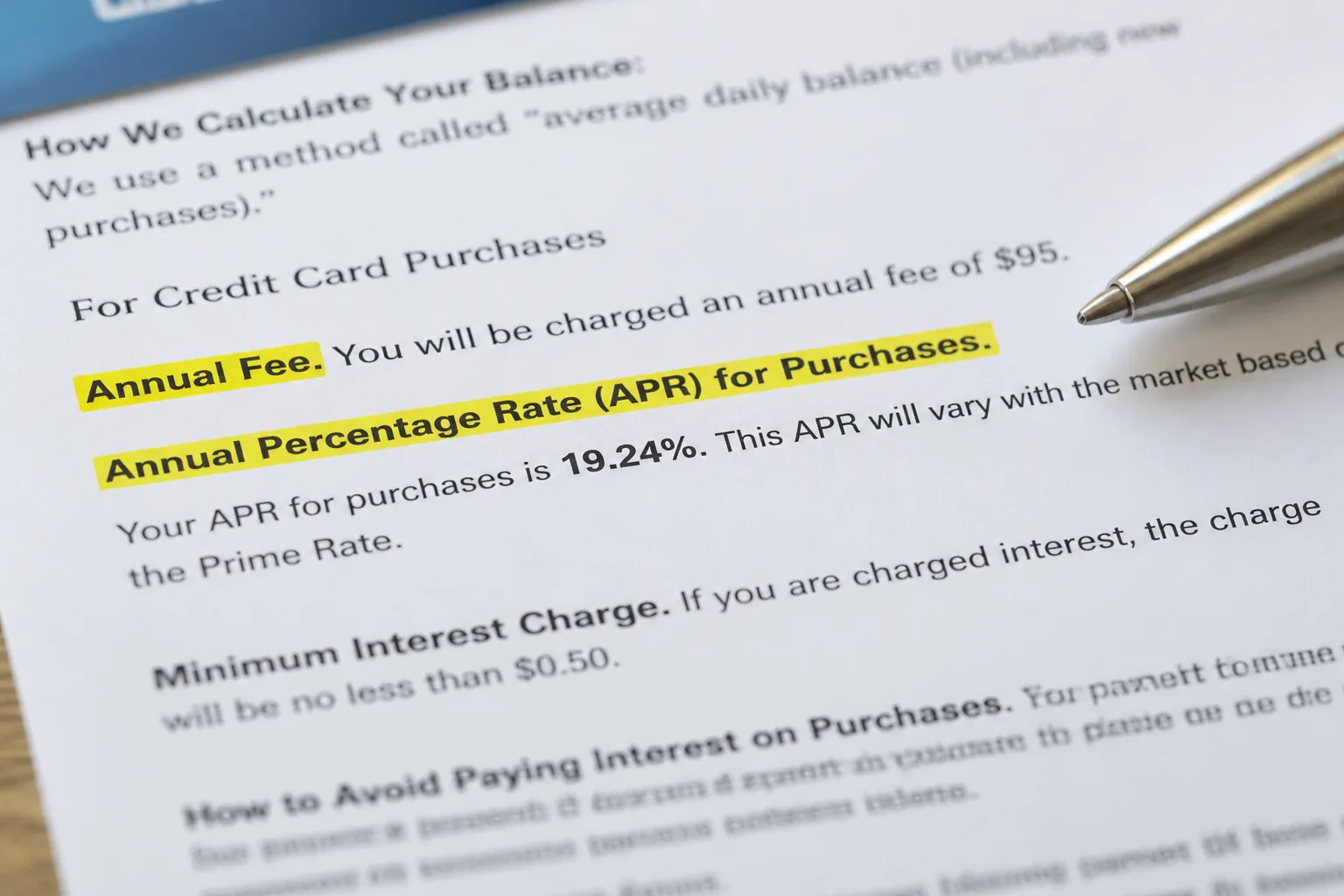

Use net value, not hype. That means rewards earned minus annual fee, then adjusted for redemption value and interest risk. If you carry a balance at 22% APR, rewards can disappear in one month. Period.

| Card type | Typical annual fee | Best for | Watch out for |

|---|---|---|---|

| Flat-rate cash back | $0-$95 | Simple spending | Fewer premium perks |

| Grocery/gas/dining cash back | $0-$250 | Households with clear categories | Caps like $6,000 a year |

| Travel card | $95-$550 | Frequent flyers | Points values vary |

| Hotel/airline card | $0-$150 | Loyal brand users | Weak value outside that brand |

A practical seven-card mix would usually include names readers know: Citi Double Cash, Wells Fargo Active Cash, Blue Cash Preferred, Chase Sapphire Preferred, Capital One Venture, Amex Gold, and a co-branded airline or hotel card. Some earn 2% flat cash back, some give 3x to 4x on dining or groceries, and some lean on transfer partners for outsized travel value. That last part can be great, but only if you’ll actually learn the system, right?

Next comes the part most reviews rush past: matching the card to real life.

03 What your spending says about the winner

Picture Maya in Columbus spending $700 a month on groceries, $220 on gas, and maybe $80 on flights all year. She probably gets more value from category cash back than from travel points. Now picture Daniel in Seattle, on the road twice a month, booking hotels for work and eating out four nights a week. His math flips.

Three quick matches:

- Flat 2% cash back: best for mixed spending and low-maintenance habits

- Grocery/dining cards: best for families and city spenders

- Flexible travel points: best for travelers who redeem through transfer partners

I’ve seen people chase 60,000-point welcome offers and ignore the obvious. If your monthly budget is steady and your redemptions are random, simplicity often wins by year two.

See our guide on travel rewards points

Quick recap: compare earn rate, annual fee, redemption value, and whether you’ll use the credits. Miss one of those four, and the “best” card can turn mediocre fast.

04 The fine print that quietly changes the score

Here’s the part issuers tuck behind the sparkle. Some grocery cards exclude Walmart and Target. Some bonus categories cap earnings at $6,000 a year. Travel portals can give 1.25 cents per point in one setup and less in another. That gap matters.

A reward isn’t worth face value if redemption rules cut it in half.

Look at these four details before you apply:

- Redemption floor: cash back at 1 cent per point is clean and easy.

- Category limits: bonus rates often stop after a fixed annual spend.

- Foreign transaction fees: usually 0% on better travel cards.

- APR and balance habits: one carried balance can wipe out months of rewards.

Related: budgeting basics that make rewards work

Once you do that, the final choice usually narrows to two cards, not twenty.

05 My clean way to choose a card this week

If you want the least regret, start with behavior. Choose cash back if you want certainty. Choose travel points if you enjoy strategy. Choose co-branded airline or hotel cards only if you already spend with that brand several times a year.

My rule of thumb is simple, and it has held up well: if you can’t explain how you’ll redeem rewards in one sentence, skip the complicated card. That sounds harsh, maybe. Still, it saves people real money.

Do these 3 things today:

- Check the last 3 months of spending and total each major category

- Estimate first-year rewards minus the annual fee

- Read the redemption and category exclusions before applying

Good rewards cards feel boring after setup. That’s usually a good sign.

The best value rarely comes from the loudest offer. It comes from a card that fits your routine in January, still works in July, and doesn’t punish you with hidden trade-offs by December. That’s the card worth keeping.