If summer spending always seems to hit at once, you’re not imagining it. A few smart moves with dividend income and high-yield savings can help you cut debt before the real money drain starts.

01 The summer money squeeze starts earlier than you think

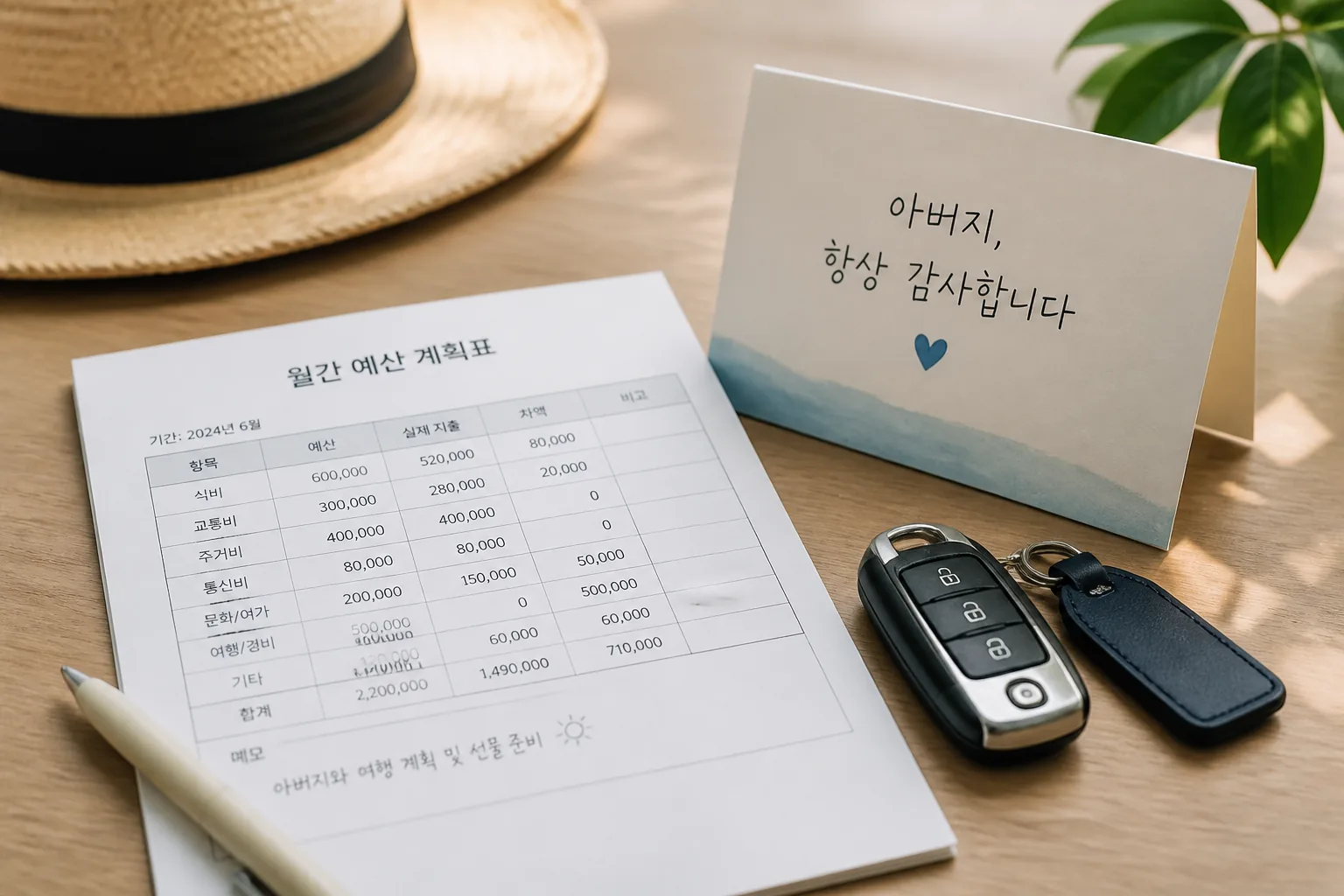

Ever look up in mid-June and wonder where $600 went? Between Father’s Day gifts, gas for road trips, and Prime Day wish lists, summer spending can hit fast.

The short version: pay off high-interest debt first, stash near-term cash in a high-yield savings account, and stop treating dividends like free spending money. When I’ve mapped this out with friends, the biggest surprise was always the math: a savings account earning 4.00% APY feels good, but a credit card charging 24.99% APR is still winning by a mile.

If you need a parallel read,

read more about the best debt payoff methods

can help you choose the right system. And if summer shopping is your weak spot,

see our guide on building a realistic monthly budget

pairs well with this plan.

A 4% return helps. A 25% interest charge hurts faster.

That gap is why the first move matters more than the fun stuff, and the next section is where most people get it wrong.

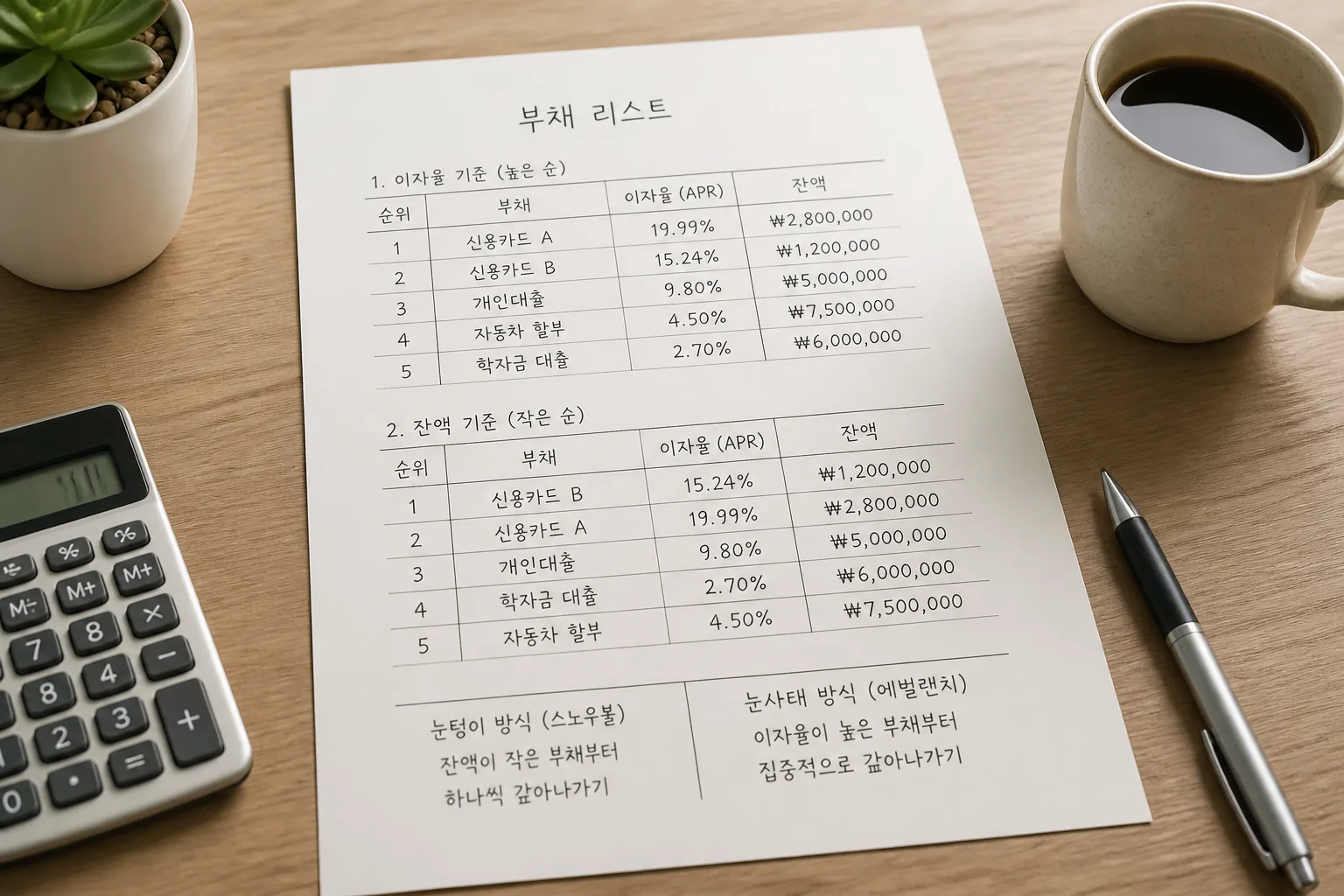

02 Avalanche or snowball? Pick the one you’ll actually stick with

Here’s the real debate. Debt avalanche targets the highest APR first, which usually saves the most money. Debt snowball attacks the smallest balance first, which gives faster emotional wins. Both work. The bad plan is the one you quit after 18 days.

Say you have a $4,000 card at 27%, a $1,200 card at 19%, and a $600 store card at 0% promo ending in August 2026. Avalanche says crush the 27% balance first. Snowball says wipe out the $600 balance, then the $1,200 card, then the big one. A friend of mine in Columbus used snowball in 2025 because seeing one balance hit zero kept him locked in. Honestly, that made sense.

Quick recap:

- Avalanche = less interest paid

- Snowball = quicker motivation

- Promo APR debt = watch the deadline like a hawk

The strategy is only half the story, though. The cash source matters just as much.

03 Why dividend income works better as a weapon than a reward

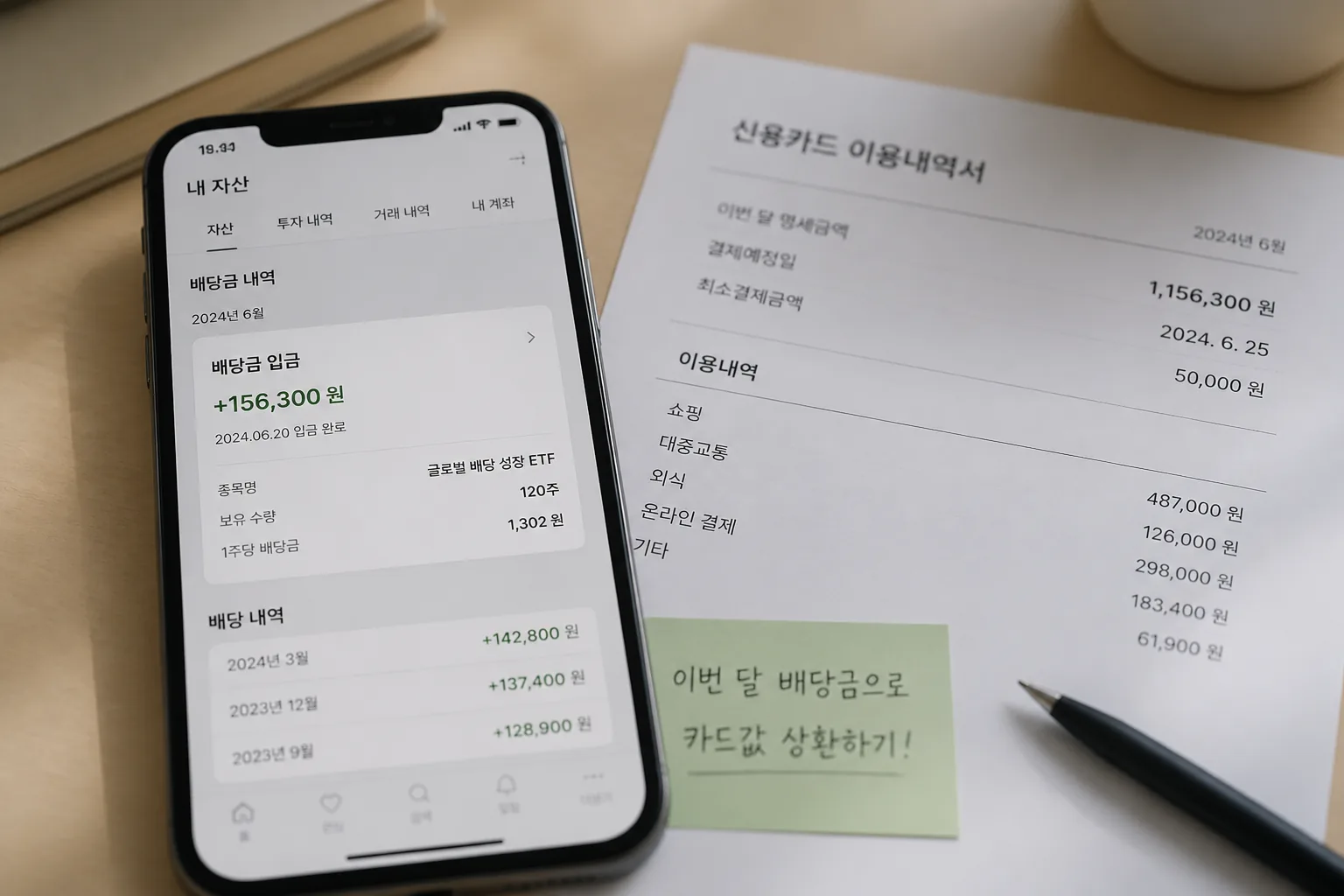

Dividend income has a funny way of disappearing. A $38 payout here, $64 there, and suddenly it’s lunch, golf balls, or one-click deals. But if your goal is lower stress by July 2026, dividends work best as targeted debt ammo.

Picture someone earning about $45 a month in dividends from a taxable brokerage account. Over 6 months, that’s roughly $270 before taxes. Put that toward a 22% APR balance, and you’re buying down expensive interest. Spend it on Father’s Day extras, and the card issuer gets the better trade. That’s the truth.

Treat dividend cash like a transfer, not a treat.

related: dividend investing basics for beginners

Of course, you still need cash for near-term plans. That’s where savings can help—if you use it carefully.

04 A high-yield savings account helps, but only for the right money

A high-yield savings account, or HYSA, is great for short-term spending you know is coming: a $250 Father’s Day budget, a $900 weekend trip, or a $400 Prime Day reserve. Put simply, this is parking money, not magic.

At 4.00% APY, $2,000 set aside for 3 months earns roughly $20 before taxes. Nice? Sure. Life-changing? Not even close. If that same household carries $2,000 on a card at 24% APR, the interest cost can outrun that savings gain fast. That mismatch trips people up every year.

Use the HYSA for money you’d otherwise spend soon anyway. Don’t use it as an excuse to carry revolving debt. Period.

- Vacation fund: yes

- Father’s Day gift cash: yes

- Emergency buffer: yes

- Ongoing card balance while chasing yield: no

Once you separate payoff money from spending money, Prime Day stops being a financial ambush.

05 Your 3-step plan before Father’s Day and Prime Day

Here’s the part to do today, not next Saturday.

- List every debt by APR, balance, and promo end date in one note on your phone.

- Open one HYSA and label three buckets: Father’s Day, vacation, Prime Day 2026.

- Auto-send dividend payouts and extra cash to one target debt until the highest-cost balance is gone.

If you can free up even $150 a month from now through early summer, that’s $450 across 3 months.

Cut two takeout nights, pause one subscription, and sell one unused gadget. This is not glamorous. It works.

see our guide on building a starter emergency fund

Bottom line: expensive debt should lose first, seasonal spending should get a clear bucket, and dividends should have a job. Start now, and summer feels lighter. Wait until Prime Day banners hit, and you’re playing defense again.