If your savings rate hasn’t changed in a while, your money may be earning less than it should. A quick comparison can reveal where the gap really is.

| Option | Typical APY | Monthly Fee | Best Use | Watch Out For |

|---|---|---|---|---|

| Online bank HYSA | 4.00%-5.00% | $0 | Emergency funds | Transfer delays |

| Credit union savings | 3.00%-5.00% | $0 | Local service | Membership rules |

| Cash management account | 3.50%-5.00% | $0 | Brokerage users | Features vary |

| Big bank promo savings | 3.50%-4.50% | $0-$5 | Existing customers | Promo expiration |

| No-penalty CD alternative | 4.00%-5.00% | $0 | 6-12 month goals | Withdrawal terms |

01 The 0.01% trap almost nobody notices

Ever leave $10,000 in a big-bank savings account for a full year and check the interest later? The result can be almost insulting. At 0.01% APY, that balance earns about $1 in a year, while a competitive high-yield account at 4.25% APY lands closer to $425 before taxes. That’s not a rounding error. That’s lunch money versus a car payment.

If you’re searching for a high yield savings account comparison, the headline rate matters, sure, but it isn’t the whole story. I’ve seen readers chase the top APY, move money twice in 6 months, then realize the app was clunky, transfers took 3 business days, or the rate fell fast.

See our guide on building a simple savings and investing plan →

The smart move is matching the account to the job.

A savings account should fit your life, not just a leaderboard.

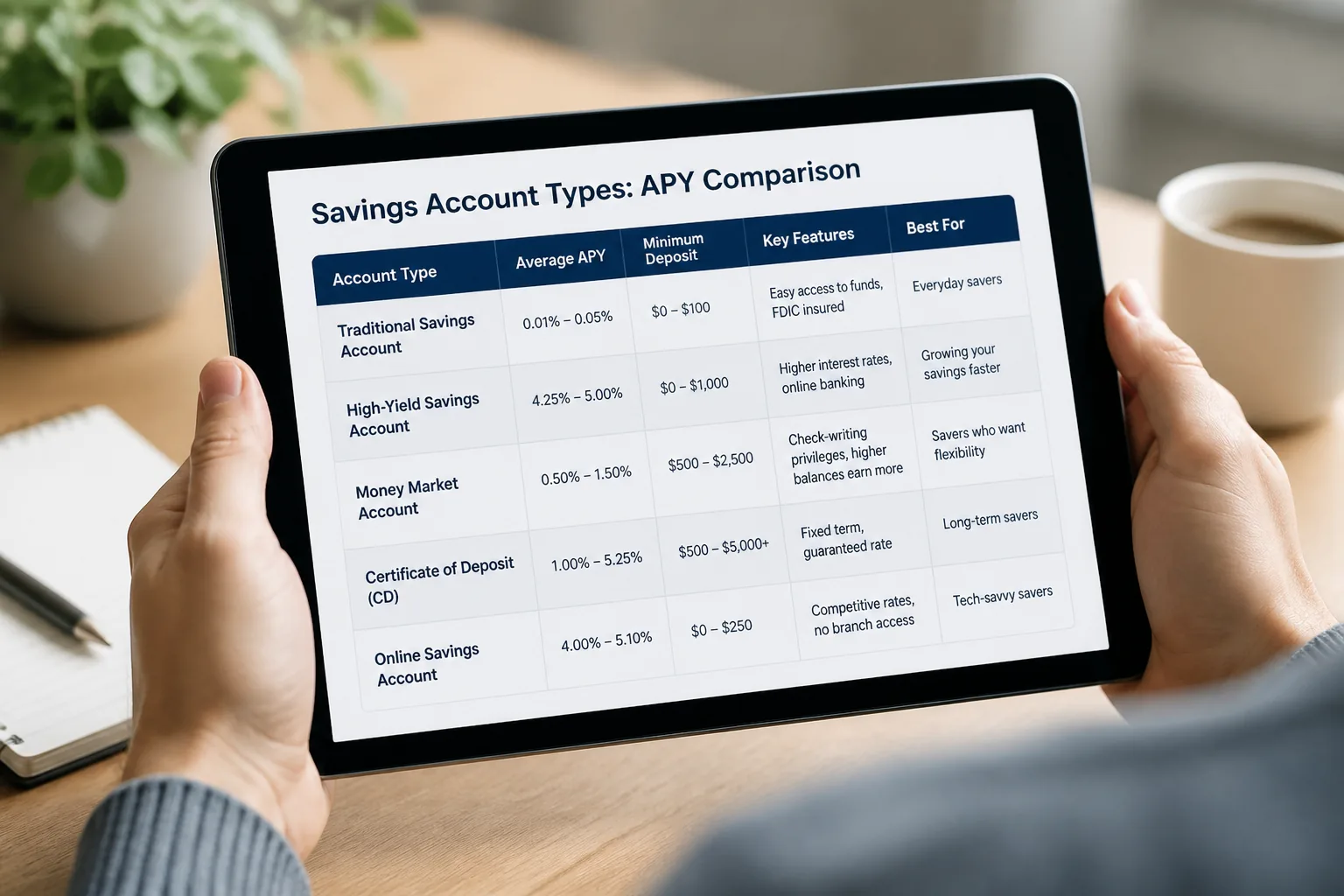

02 7 accounts worth a close look right now

Quick comparison first:

| Account type | Typical APY range | Monthly fee | Best for |

|---|---|---|---|

| Online bank HYSA | 4.00%-5.00% | $0 | Highest yield seekers |

| Credit union savings | 3.00%-5.00% | Usually $0 | Members who want service |

| Cash management account | 3.50%-5.00% | $0 | Savers who also invest |

| Big bank promo savings | 3.50%-4.50% | Often avoidable | Existing bank customers |

| Kids/goal savings account | 2.00%-4.00% | $0 | Families teaching saving |

| No-penalty CD alternative | 4.00%-5.00% | $0 | Money needed in months |

| Joint emergency fund HYSA | 4.00%-5.00% | $0 | Couples pooling cash |

A friend of mine in Chicago kept her emergency fund at a branch bank earning almost nothing until late 2024. She switched to an online HYSA at 4.40% APY and started earning roughly $36 a month on a $10,000 balance. Not life-changing, but very real.

Next comes the part banks advertise in smaller print.

03 What nobody tells you about the highest APY

That flashy 5.00% APY can come with strings. Some accounts require direct deposit, debit card activity, a linked brokerage balance, or a promotional window that lasts 3 months. Honestly, this is where people get tripped up.

Three details deserve more attention than the banner rate:

- Rate stability: Was the APY competitive for 12 months, or just 12 days?

- Transfer speed: Can you move money in 1 business day or 4?

- Balance rules: Does the top APY stop after $5,000 or kick in only above $25,000?

The best account on paper can be the worst account in practice.

So who should pick what? That’s where the comparison gets useful.

04 Match the account to the money goal

If you’re saving your first $1,000 emergency fund, keep it simple: an online HYSA with no fee, no minimum, and fast transfers. If you’re parking $10,000 for a house repair in 6 to 12 months, a no-penalty CD alternative or a steady HYSA can make more sense than chasing every weekly rate bump.

For couples, a joint HYSA works well for shared bills and emergency cash. For investors already using Fidelity, Schwab, or another brokerage, a cash management account can feel smoother because transfers stay inside one login. Like keeping your keys, wallet, and phone in the same bowl by the door. Less friction, fewer mistakes.

Quick recap:

- Best pure yield: online HYSA

- Best convenience: cash management account

- Best for local service: credit union savings

- Best for short-term goals: stable HYSA or no-penalty CD

Related: credit card comparison for everyday cash flow

One last piece can save you from opening the wrong account tonight.

05 A simple 10-minute checklist before you open one

Start here today:

- Check the current APY and whether it’s promotional

- Confirm FDIC or NCUA insurance coverage

- Read the transfer limits and expected ACH timing

- Make sure monthly fees are $0 or clearly avoidable

- Test whether the mobile app and alerts feel usable

When I compare accounts, I ask one plain question: Would I trust this setup at 11 p.m. during a real emergency? That usually cuts through the marketing fast.

Read more about emergency fund basics and target amounts

Bottom line: the best high-yield savings account is the one that pays a strong rate, keeps fees at zero, and lets you reach your cash without drama. Pick the account that fits your timeline, fund it this week, and set one automatic transfer. Small move. Better outcome.