If you’re comparing life insurance plans and they all look the same, that’s exactly where costly mistakes happen. The small details usually decide which policy actually protects your family.

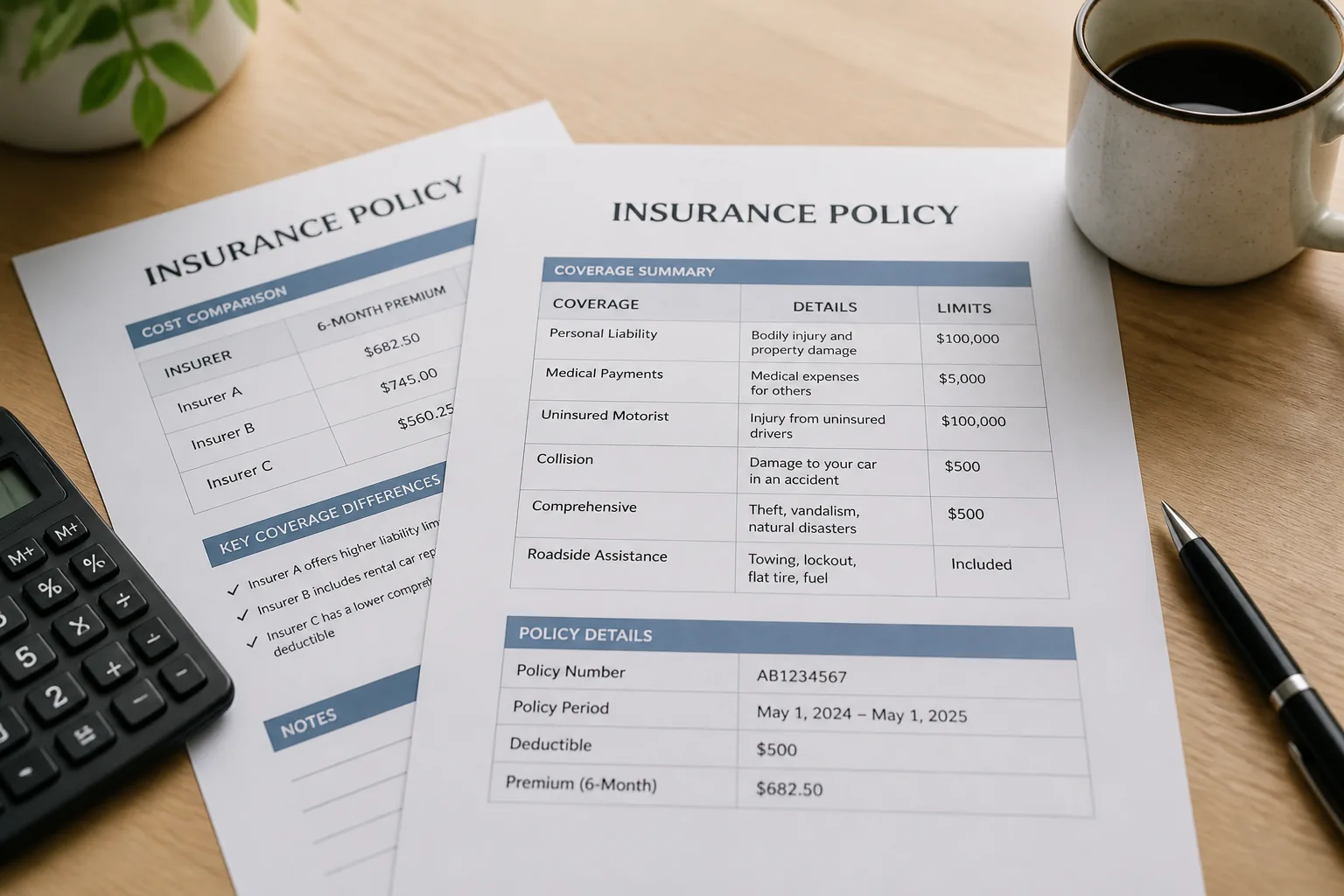

| Policy | Monthly Cost | Coverage | Term Length | Cash Value |

|---|---|---|---|---|

| 20-year term | $18-$30 | $500,000 | 20 years | No |

| 30-year term | $25-$45 | $500,000 | 30 years | No |

| Whole life | $250-$450 | $500,000 | Lifetime | Yes |

| Guaranteed issue | $40-$70 | $25,000 | Lifetime | Very limited |

| Final expense | $35-$80 | $15,000 | Lifetime | No/limited |

01 Life insurance gets expensive fast when you buy the wrong kind

Ever price a policy at lunch and wonder why one quote says $18 a month while another lands near $240? That gap is where most people get lost. Life insurance comparison sounds simple, but the fine print changes everything: term length, cash value, medical exams, and rider costs.

When I’ve walked friends through quotes, the same pattern shows up every time. A 30-year-old parent looking for $500,000 in coverage usually cares about one thing first: keeping the mortgage and kids covered if the paycheck disappears. That’s why term life often wins on price.

read more about building a family financial safety net

The cheapest policy is not the best deal. The best deal is the one that still fits your life five years from now.

The short version? Term life buys more coverage for less money, while permanent policies trade low cost for long-term features. The numbers make that painfully clear, and that’s where we’re headed next.

02 5 policy costs compared without the sales pitch

Here’s a practical snapshot using common market ranges for a healthy non-smoker. Rates vary by age, sex, health, and insurer, but these examples are close enough to be useful.

| Policy type | Sample monthly cost | Coverage period | Cash value |

|---|---|---|---|

| 20-year term, $500k, age 30 | $18-$30 | 20 years | No |

| 30-year term, $500k, age 30 | $25-$45 | 30 years | No |

| Whole life, $500k, age 30 | $250-$450 | Lifetime | Yes |

| Guaranteed issue, $25k, age 50 | $40-$70 | Lifetime | Very limited |

| Final expense, $15k, age 60 | $35-$80 | Lifetime | No/limited |

Term life is usually the value play for income replacement, debt payoff, and child-raising years. Whole life costs far more because part of your premium funds lifelong coverage and cash value. Guaranteed issue skips the exam, which sounds great at 8 p.m. after a long day, right? But the tradeoff is higher cost per dollar of coverage.

The real question isn’t just price. It’s what that price is buying.

03 What nobody tells you about term vs. whole life

Term life covers a risk window. Whole life covers a lifetime. That one sentence clears up half the confusion.

Think of term life like renting a safety net for 20 or 30 years. If your kids are 4 and 7 today, a 20-year term often lines up neatly with the years your income matters most. I’ve seen this work well for households with a mortgage, one main earner, and a tight monthly budget. Clean. Affordable. Done.

Whole life works differently. Part insurance, part forced-savings bucket. For high-income households, estate planning cases, or people who have already maxed out retirement accounts, that structure can make sense. But for the average buyer comparing bills in a kitchen chair at 9:30 p.m., the premium can feel brutal.

Buy insurance for protection first. Buy complexity only if you truly need it.

Before you choose, there are three fine-print items that can change the deal more than the headline rate.

04 Three details that change the quote more than you expect

First, underwriting rules. One company may rate mild asthma as standard, while another bumps you into a pricier class. Same person. Same age. Different result. That’s why two quotes can be $12 apart each month for identical coverage.

Second, riders. Waiver of premium, child term, and accelerated death benefit riders add value, but they also add cost. A friend of mine added riders without checking the math and ended up 22% above the base quote. Useful? Sure. Automatic? No.

Third, coverage amount. A common shortcut is 10 to 12 times annual income, then adjust for debts, childcare, and savings. If you earn $80,000 and carry a $280,000 mortgage, $500,000 may be light. $1 million may be closer, honestly.

see our guide on protecting a mortgage with insurance

Quick recap:

- Compare the same coverage across at least 3 insurers

- Check whether the quote includes riders

- Match the term length to your biggest financial obligations

One last piece matters most: what to do today, before another quote tab gets ignored.

05 Start here if you want the shortlist fast

If you want a clean decision, keep it boring. Price term life first, then compare permanent coverage only if you have a clear long-range reason. That alone saves a lot of people from buying a fancy product they never needed.

- Pull your income, debts, mortgage balance, and savings totals today.

- Get 3 matched quotes for 20-year and 30-year term coverage.

- Ask one direct question: "What changes this premium at renewal or after underwriting?"

Related:

read more about estate planning basics before buying permanent coverage

For most households, term life is the practical answer. For a smaller group with estate goals or lifelong dependents, permanent insurance deserves a closer look. Either way, compare the same numbers, read the riders, and don’t let a low headline premium distract you from weak coverage. That’s the move.