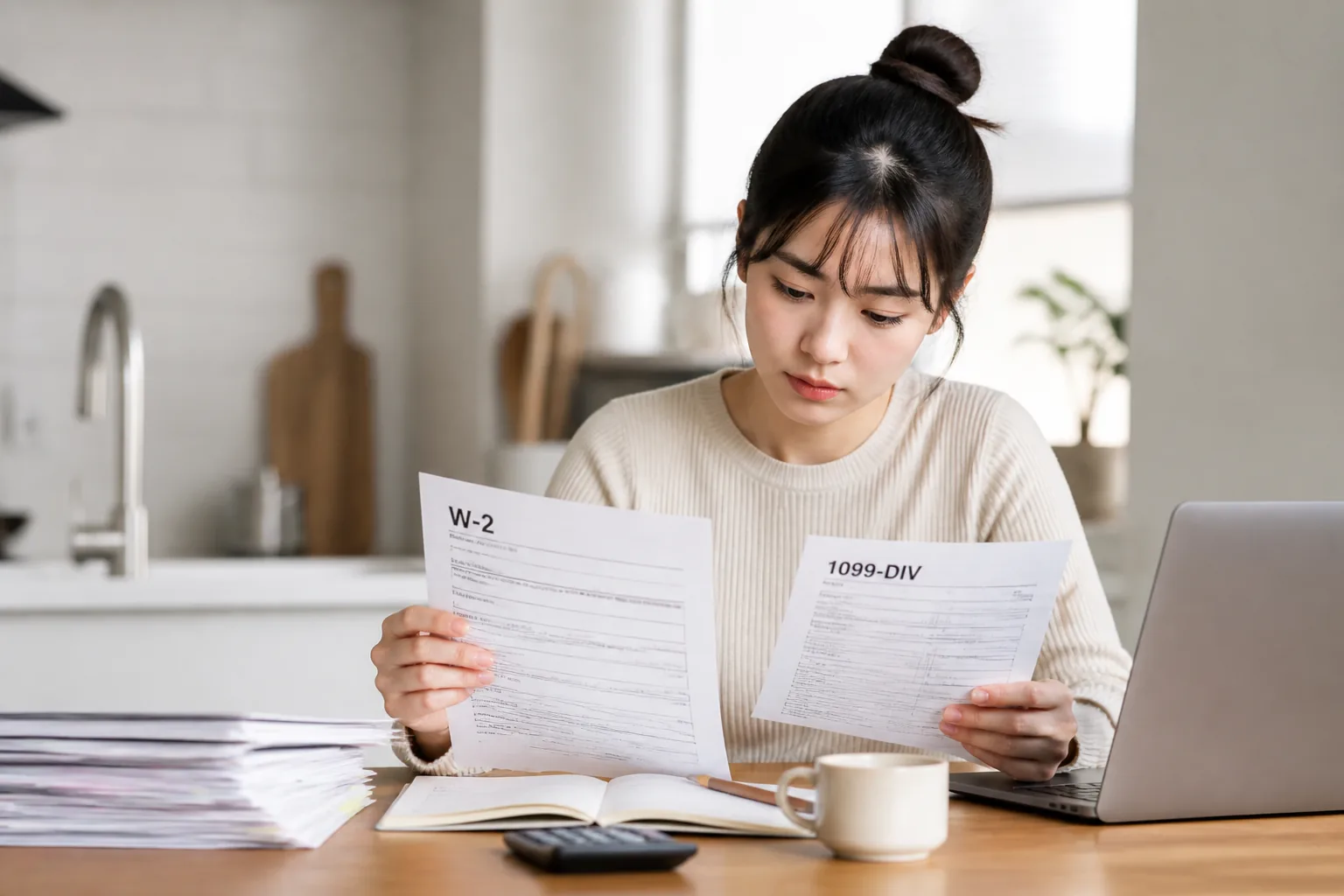

Just graduated and already juggling summer pay, dividend income, and insurance changes? That combo can make a basic tax return feel a lot less basic.

| Software | Price | Best For | Key Strength | Main Drawback |

|---|---|---|---|---|

| TurboTax | Higher tier in many cases | First-time filers wanting guidance | Best interview flow | Can get expensive fast |

| H&R Block | Mid-to-high | Filers wanting office backup | Strong support options | State costs may add up |

| FreeTaxUSA | Low-cost federal | Most grads with W-2 + 1099-DIV | Best value | Plain interface |

| Cash App Taxes | $0 in many cases | Budget-focused simple returns | Free federal and state | Less hand-holding |

| TaxSlayer | Mid-range | Cost-conscious filers needing support | Solid balance | Less polished UX |

02 Your first “easy” tax year rarely stays easy

Ever think, “I only had a summer job, how hard can this be?” Then May rolls around, a 1099-DIV lands in your inbox, your Marketplace premium changed twice, and suddenly the return feels like IKEA furniture with one missing screw.

That’s the spot a lot of recent grads hit in 2026. A friend of mine in Chicago had a W-2 from a campus job, a second W-2 from a July internship, $184 in dividend income from a brokerage app, and one messy health insurance switch after turning 26. Simple on paper, annoying in real life.

read our guide to first-time tax filing

This review looks at TurboTax, H&R Block, FreeTaxUSA, Cash App Taxes, and TaxSlayer for that exact mix. Pricing and features can change by filing season, so treat these as May 2026 snapshots, not eternal truth.

The trap isn’t the summer job. It’s the extra form you forgot was coming.

And that extra form is where the price gap starts to matter.

03 5 picks that make sense, depending on your mess level

Here’s the short list:

| Software | Federal price* | Best for | Watch out for |

|---|---|---|---|

| TurboTax | Higher tier in many cases | First-timers who want guidance | Price jumps with investments/ACA |

| H&R Block | Mid-to-high | Good interview flow, in-person backup | State returns can add up |

| FreeTaxUSA | Low-cost federal | Best value for most grads | Interface feels plain |

| Cash App Taxes | $0 federal/state in many cases | Budget filers with simpler returns | Less hand-holding |

| TaxSlayer | Mid-range | Solid balance of cost and support | Less polished than top rivals |

When I test tax software, I care about three things: price, form coverage, and how quickly the app flags mistakes. FreeTaxUSA usually comes out ahead for recent grads because it handles dividend income and common credits without making you pay luxury pricing. TurboTax still has the cleanest “what happened this year?” flow. Honestly, that part is hard to beat.

The health insurance piece, though, is where a cheap return can turn expensive fast.

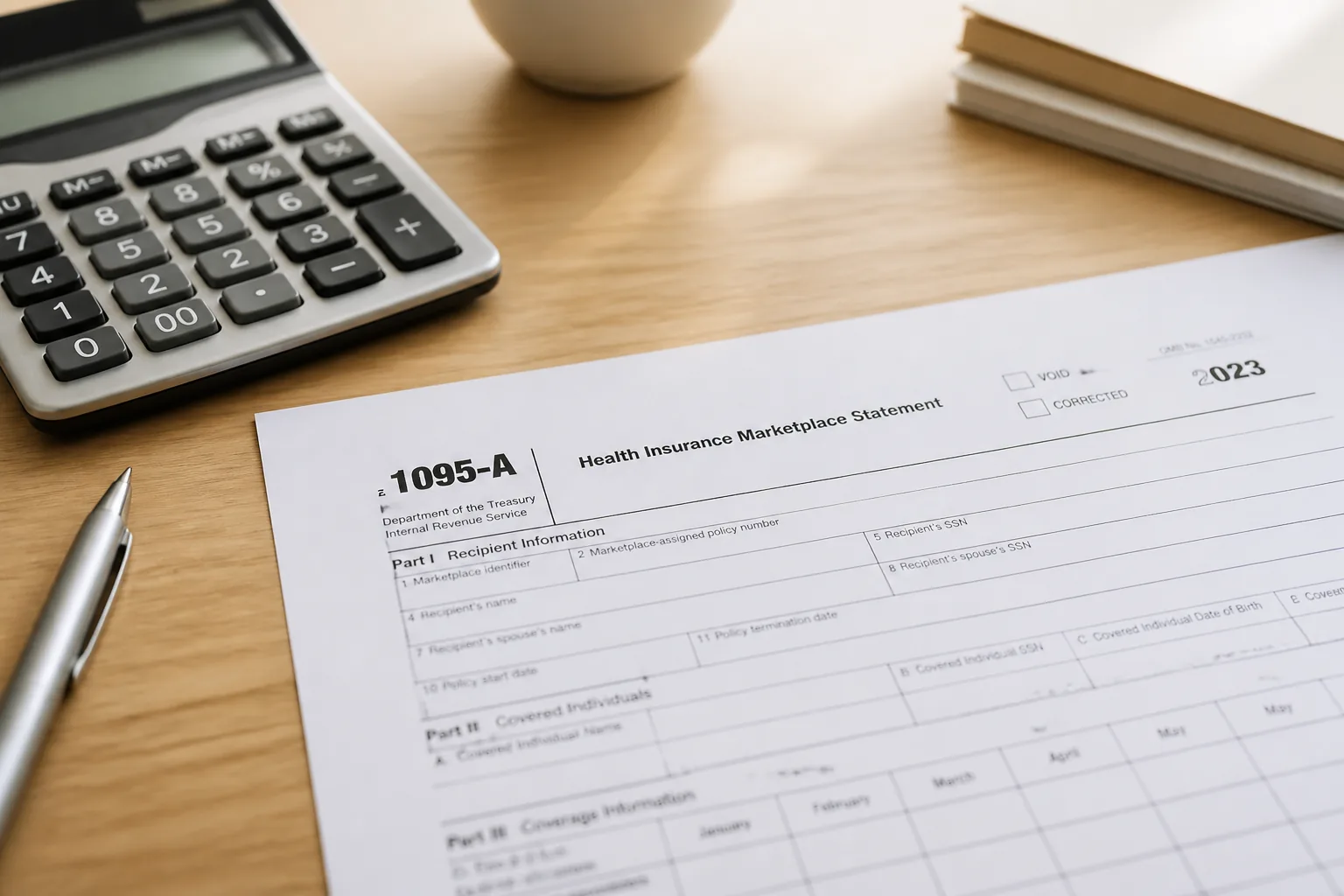

04 The health insurance wrinkle nobody warns grads about

Turned 26 in 2025? Moved off a parent plan? Bought coverage on HealthCare.gov for three months, then switched jobs in August? That’s where Form 1095-A and the Premium Tax Credit enter the chat.

If advance premium credits were paid for your plan, your software has to reconcile them on Form 8962. Miss that, and your return can stall. The IRS has been clear on this for years, and HealthCare.gov spells it out too. A lot of “free” products either push you into a paid tier here or make the interview clunky.

One insurance change in September can affect a return filed eight months later.

Then there’s the investment income piece, which looks tiny until it isn’t.

05 A $63 dividend can still change your filing choice

Dividend income feels small because, for many grads, it is small. Maybe $63 from Schwab, $112 from Fidelity, or $240 from a Robinhood account started during senior year. But a 1099-DIV still needs to be entered correctly, especially if ordinary and qualified dividends are split.

That’s why I’d break the software picks like this:

- FreeTaxUSA: best value for W-2 + 1099-DIV + basic credits.

- TurboTax: best if you want the smoothest guidance.

- H&R Block: strong middle ground, especially if you may want office help.

- TaxSlayer: decent budget alternative with fair support.

- Cash App Taxes: best if cost is the only issue and your return is still pretty clean.

see our beginner’s guide to dividend income

related: how ACA premium changes affect your budget

Quick recap:

- Best value: FreeTaxUSA

- Best guidance: TurboTax

- Best free bet: Cash App Taxes

- Best backup option: H&R Block

What should you do today, before you lose another Saturday to this stuff?

06 Do these 3 things before you hit file

First, gather every form in one folder: W-2s, 1099-DIV, 1095-A, and any 1098-T if school credits still apply. Ten minutes now can save an hour later.

Second, price-check two platforms before entering everything. Start with FreeTaxUSA or Cash App Taxes, then compare with TurboTax or H&R Block if your return gets weird. I’ve seen a $40 return become a $120 return just because one extra form appeared. That stings.

Third, look at withholding from that summer or temp job. Short-term employers often withhold in a way that feels random, especially if you worked only 8 to 10 weeks.

Pick software based on your forms, not the ad you saw first.

If your 2025 tax year included a job change, ACA coverage, or even modest dividend income, don’t assume the cheapest option is the best fit. But don’t overpay for hand-holding you don’t need either. Start with the forms. Match the software to the forms. That’s the move.