Stuck between an index fund and an ETF? The difference looks small on paper, but it can affect fees, taxes, and how easy investing feels.

| Feature | Index Mutual Fund | ETF | Best For |

|---|---|---|---|

| Pricing | Once after market close | All day during market hours | ETF for timing flexibility |

| Minimum investment | Often $1,000 to $3,000 | Usually 1 share or fractional share | ETF for small starters |

| Automation | Usually very easy | Broker-dependent | Index fund for hands-off investing |

| Taxes in taxable accounts | Can distribute gains | Often more tax-efficient | ETF for taxable accounts |

| Trading costs | No spread | Bid-ask spread applies | Index fund for simplicity |

01 The fast answer before you overthink it

Ever stare at two funds that own the same 500 stocks and wonder why one gets a ticker symbol and the other doesn’t? That’s where a lot of new investors get stuck.

Here’s the short version: index funds and ETFs can be built from the exact same index, like the S&P 500, but they behave differently once you buy them. An index mutual fund prices once each trading day after 4 p.m. Eastern. An ETF trades all day, minute by minute, like Apple or Tesla stock. That one detail changes convenience, taxes, and even who each option fits best.

I’ve walked friends through this choice inside both Roth IRAs and taxable brokerage accounts, and the confusion is almost always the same: they focus on the expense ratio and miss the rest of the bill. Spreads, minimums, and tax drag matter too.

Read our guide to investment basics first

and this comparison gets much easier.

Same holdings, different wrapper. That’s the real story.

Next, let’s get into the first difference people actually feel on day one.

02 1 big difference: how you buy them

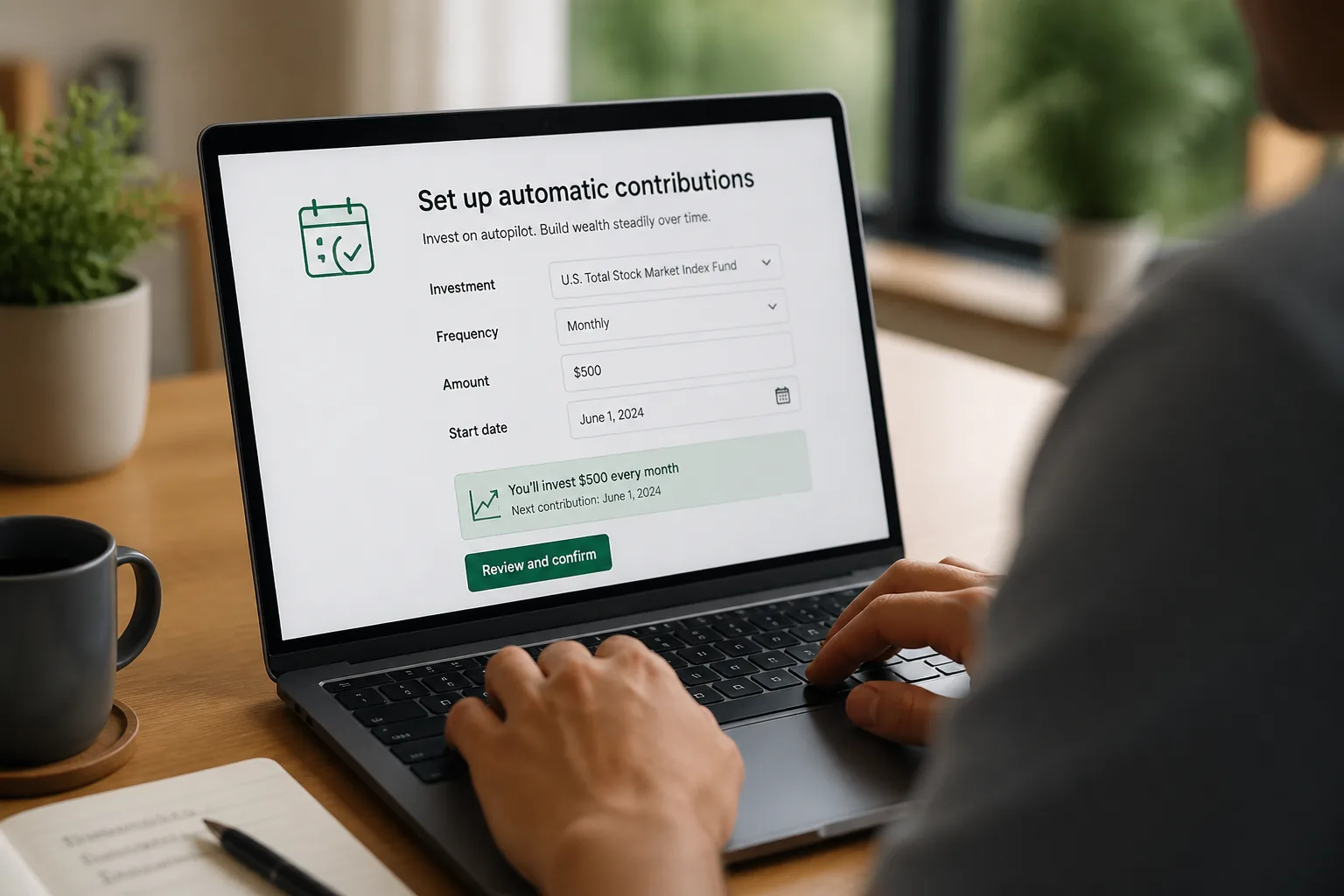

Index mutual funds usually let you invest in dollar amounts, automate weekly deposits, and forget about it. Many brokers also set minimums. Vanguard’s mutual fund minimum for many investor shares has often been $3,000, while plenty of ETFs start with the price of 1 share, or even less if your broker offers fractional shares.

ETFs trade intraday, which sounds exciting until you realize long-term investors rarely need that flexibility. If you’re building a 30-year retirement account, buying at 10:17 a.m. instead of 4:00 p.m. won’t make or break you. But if you want limit orders, tighter control, or easy portability across brokers, ETFs feel smoother.

Think of it like groceries. An index fund is a standing weekly order. An ETF is grabbing items one by one as prices move down the aisle. Same food, different shopping experience.

- Choose index funds for automatic investing

- Choose ETFs for trading flexibility

- Check fund minimums before you decide

The buying process is only half the picture, though. Costs get more interesting.

03 The cost gap isn’t just the fee on the label

A lot of investors compare expense ratios and stop there. Fair enough, but that misses two real-world costs: bid-ask spreads and taxes.

An S&P 500 index fund might charge 0.03% a year. An S&P 500 ETF might also charge 0.03%. Looks like a tie, right? Not always. ETFs have a spread, sometimes just 1 cent, sometimes more in thinly traded funds. Mutual funds skip that spread but may create taxable capital gains distributions more often, depending on structure and turnover.

For taxable accounts, ETFs often have a tax edge because of the creation-redemption mechanism. That’s a fancy phrase for how ETF shares are exchanged behind the scenes without forcing as many taxable sales inside the fund. Honestly, this surprised a friend of mine last April when her mutual fund kicked out gains in a flat market.

The cheapest fund on paper isn’t always the cheapest fund in your account.

Quick recap:

- Expense ratio matters

- Spreads matter for ETFs

- Tax efficiency matters most in taxable accounts

That leads to the question people should ask first, not last.

04 Where each one fits best in real life

If you’re 28, contributing $400 a month to a Roth IRA, an index mutual fund is wonderfully boring. Set the transfer, reinvest dividends, move on. That friction-free routine helps more than shaving a penny off a trade. Convenience wins a lot of retirement battles.

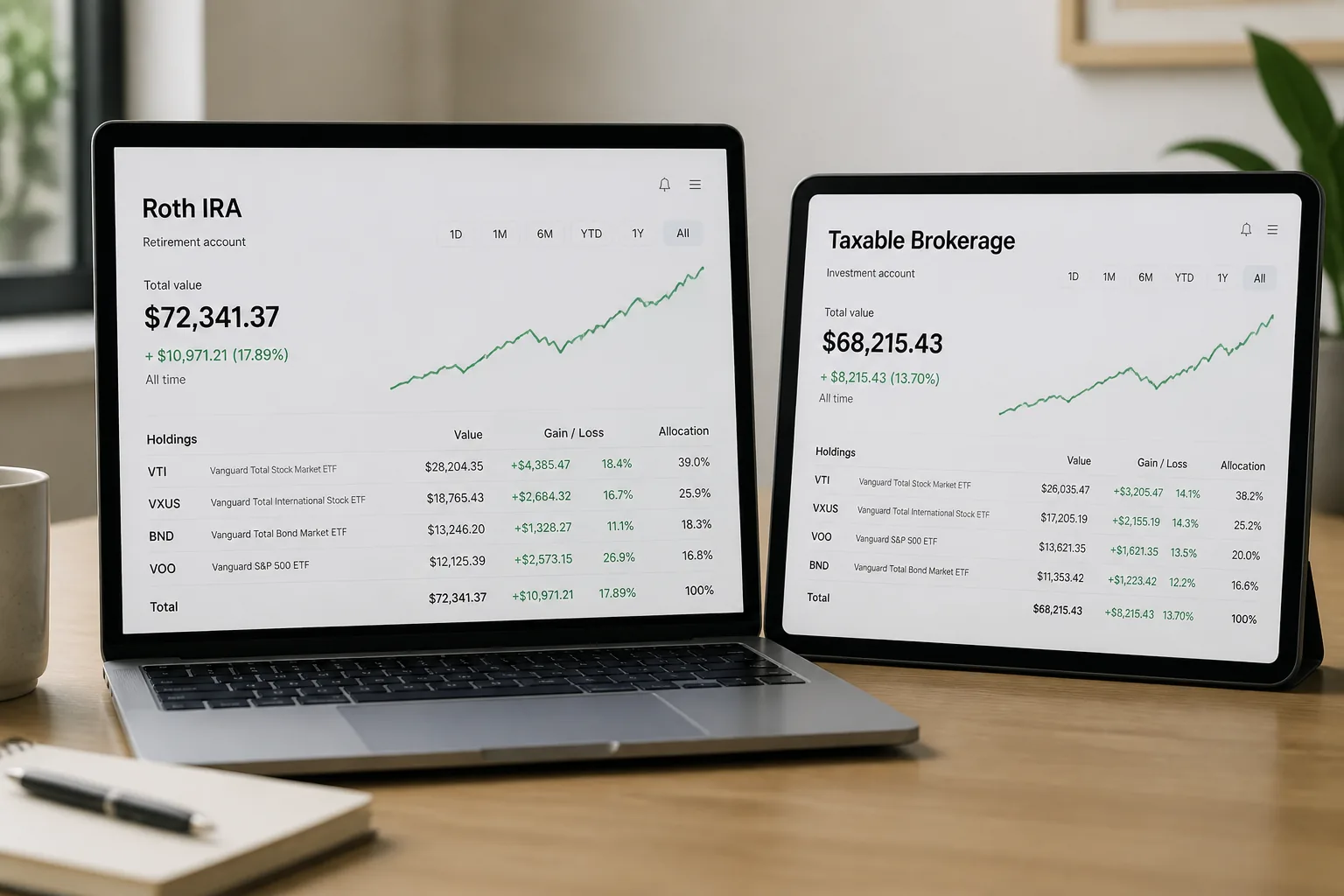

If you’re 41, already maxing retirement accounts, and investing extra cash in a taxable brokerage account, ETFs start to look better. You may want lower tax drag, no minimum, and the freedom to move between Fidelity, Schwab, or Vanguard without changing your approach. That’s where ETFs often shine.

Of course, there are exceptions. Some brokers now offer automatic ETF investing and fractional shares, which narrows the old gap.

See our Roth IRA investing guide →

if you’re deciding inside a retirement account.

Related: taxable brokerage account basics

if taxes are your bigger concern.

So which one should you buy today? Keep this final filter in mind.

05 My simple rule for choosing without regret

Here’s my rule: pick the version you’ll actually stick with for 10 years. If automation keeps you consistent, choose the index mutual fund. If tax efficiency and flexibility matter more, choose the ETF. For many investors, either choice beats waiting 6 months while cash sits idle.

Then do this:

- Decide whether the money is for a retirement or taxable account.

- Compare one index mutual fund and one ETF tracking the same index.

- Buy the simpler option and schedule the next contribution now.

Great investing usually looks a little boring and a lot consistent.

That’s the answer. Same market exposure, different mechanics. Pick the wrapper that matches your habits, and you’ll probably sleep better by next week.