If graduation money is about to land in your account, this is the fork in the road. Index fund or ETF sounds like a small choice until your first real investing decision is on the line.

| Option | Trading Style | Income Potential | Best Use |

|---|---|---|---|

| KOSPI 200 ETF | Real-time | Low to medium | Core Korea exposure |

| S&P 500 ETF | Real-time | Low | Long-term global growth |

| Korea dividend ETF | Real-time | Medium to high | Income-focused starter sleeve |

| Global dividend ETF | Real-time | Medium | Diversified dividend exposure |

| Low-cost index mutual fund | End-of-day pricing | Low to medium | Automatic monthly investing |

01 The choice looks small until real money hits the account

Ever notice how two funds can track the same market and still feel totally different once you buy them? That’s exactly where a May 2026 graduate can get tripped up. Index funds and ETFs often hold similar stocks, but the buying experience, pricing, and flexibility are not the same.

Here’s the short version: an index fund is usually priced once after the market closes, while an ETF trades during market hours like a stock. If you’re starting with 300,000 won to 1 million won before summer, that difference matters more than the marketing copy. I’ve seen beginners freeze over this, honestly, because both options sound “passive” and safe on paper.

read our beginner investing guide before your first account

What matters here is how you’ll actually behave on a Tuesday morning in June 2026. If you like automation and less temptation, index funds feel calmer. If you want live pricing and easier intraday trades, ETFs feel more natural. The next piece is where costs and dividends start to separate the two.

02 Fees, timing, and dividends: the stuff beginners usually miss

A friend of mine once bought an ETF at 9:05 a.m. just because the chart looked green. By 3:20 p.m., he regretted chasing the move. That’s the hidden issue with ETFs: convenience can invite bad habits. Index funds remove that drama because every order gets the end-of-day net asset value. Boring? Yes. Useful for beginners? Also yes.

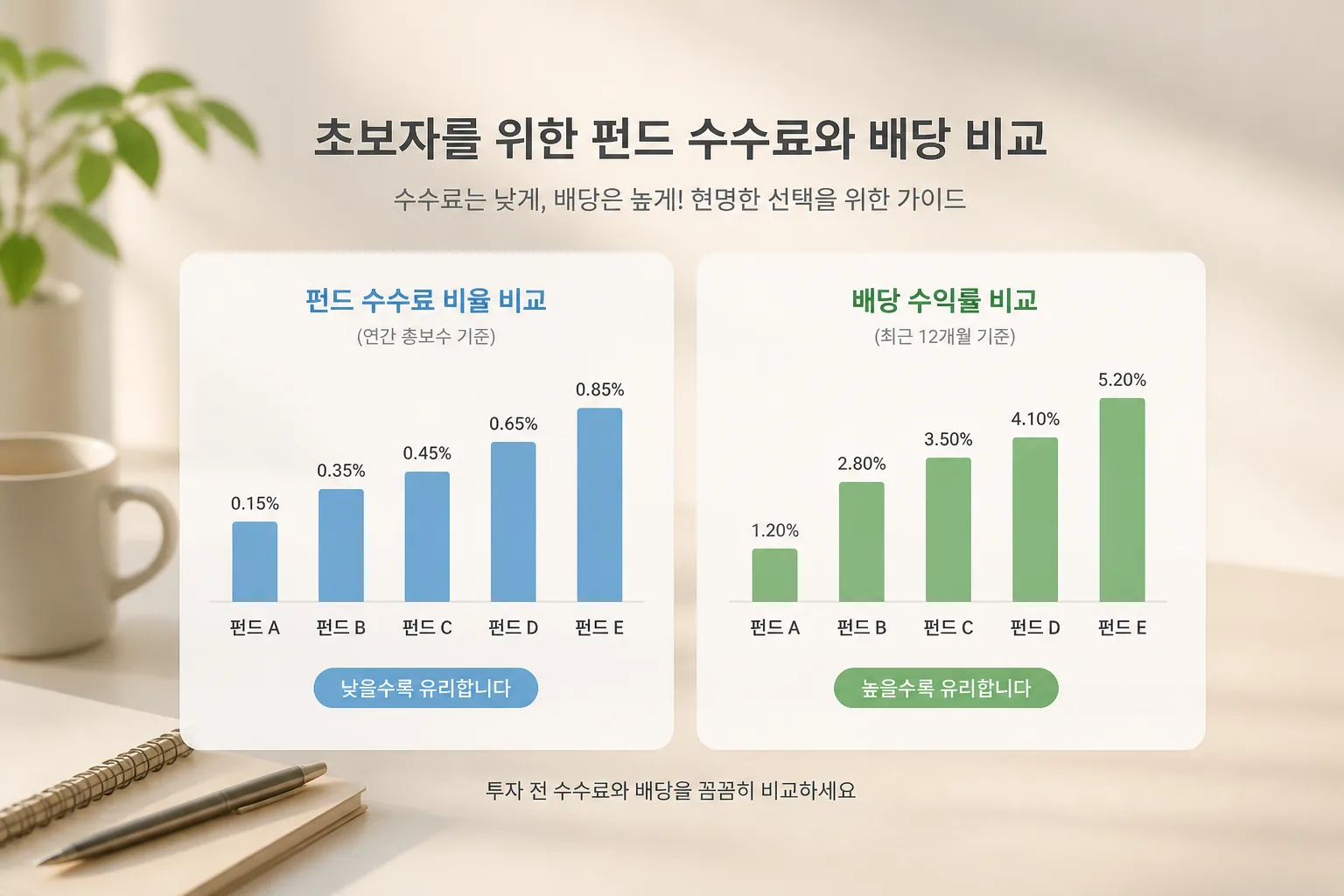

Dividend funds add another layer. NH투자증권 and 한국투자증권 both offer access to domestic dividend-focused products, but you still need to check 4 things: total expense ratio, recent distribution history, sector concentration, and trading spread if the product is an ETF. A fund yielding 4.5% can still disappoint if bank, telecom, or energy holdings dominate too heavily.

A beginner usually needs fewer choices, not fancier ones.

03 5 starter picks worth screening before summer

I’d screen these as types, not blind recommendations. Public product menus change, and brokers update lineups fast.

| Option | Best for | Watch out for | Why it fits |

|---|---|---|---|

| KOSPI 200 ETF | First-time buyers | Intraday volatility | Simple Korea large-cap exposure |

| S&P 500 ETF | Long-term growth | Currency swings | Global diversification in one trade |

| Korea dividend ETF | Income focus | Sector concentration | Cash flow mindset for beginners |

| Global dividend ETF | Balanced income | Lower growth years | Spreads risk beyond one market |

| Low-cost index mutual fund | Auto-investing | No live trading | Great for monthly discipline |

If you’re using NH투자증권 or 한국투자증권, the practical comparison is less about the logo and more about which account makes recurring purchases, fund search, and dividend records easiest to follow. Some apps feel cleaner for ETF execution; some make managed fund screening less annoying. That sounds minor until July, when you’re trying to understand where 27,000 won in distributions came from.

see our guide to building a first dividend portfolio

Next up, let’s make this choice real with two beginner scenarios.

04 Two beginner paths that make the decision easier

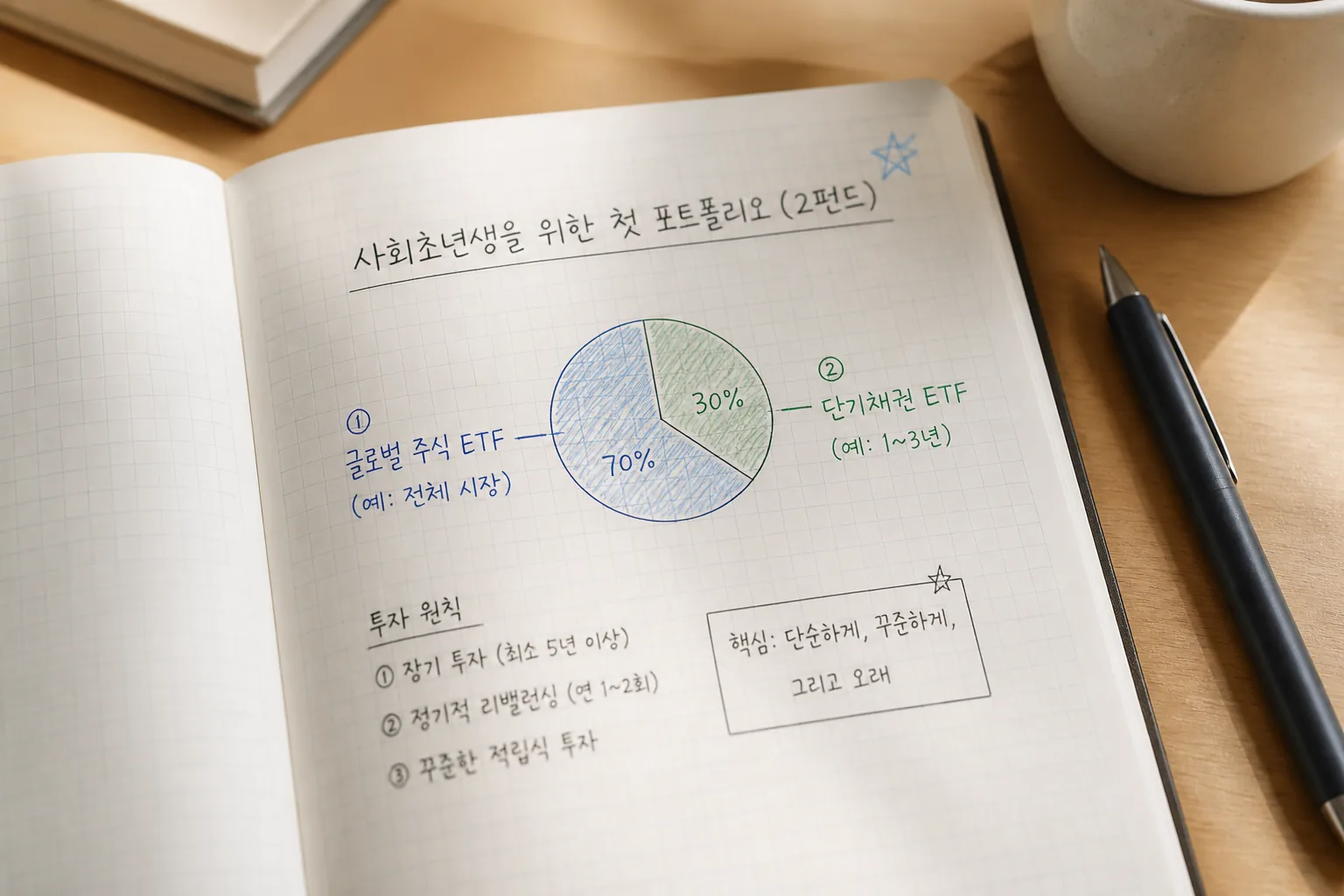

Picture Minji, graduating in May 2026, with 500,000 won now and 200,000 won monthly from a new job. She hates watching charts. For her, a low-cost index fund with automatic monthly investing probably wins. Less noise. Fewer chances to overreact. Period.

Now picture Joon, same graduation month, same starting cash, but he wants U.S. market exposure and likes placing orders himself. An ETF mix—say one broad-market ETF and one dividend ETF—could fit better. He gets live pricing, easier market access, and faster portfolio changes. Of course, there are exceptions. If Joon starts trading every dip and spike, the ETF advantage disappears fast.

The best starter fund is the one you can keep buying in August, not just in May.

05 What to do this week before summer starts

If you’re graduating in May 2026, you do not need a 9-fund masterpiece. You need a setup you’ll still understand by September. Index funds suit automation and emotional distance. ETFs suit flexibility and live trading. Dividend funds can work, but only after you check fees, concentration, and total return.

Quick recap:

- Pick index funds if you want hands-off monthly investing

- Pick ETFs if you want real-time control and broad market access

- Use dividend funds as a piece of the plan, not the whole plan

- Open your NH투자증권 or 한국투자증권 app today and compare one broad-market ETF with one low-cost index fund.

- Write down your monthly amount—100,000 won, 200,000 won, whatever is real.

- Read the fund sheet for expense ratio, top 10 holdings, and payout history before buying.

related: brokerage account features beginners should compare first

That’s the move. Keep it simple now, and your future self has a much better shot at staying invested.