Planning a Memorial Day or summer trip right after graduation? A smart rewards card can help now, while a dividend strategy builds breathing room later.

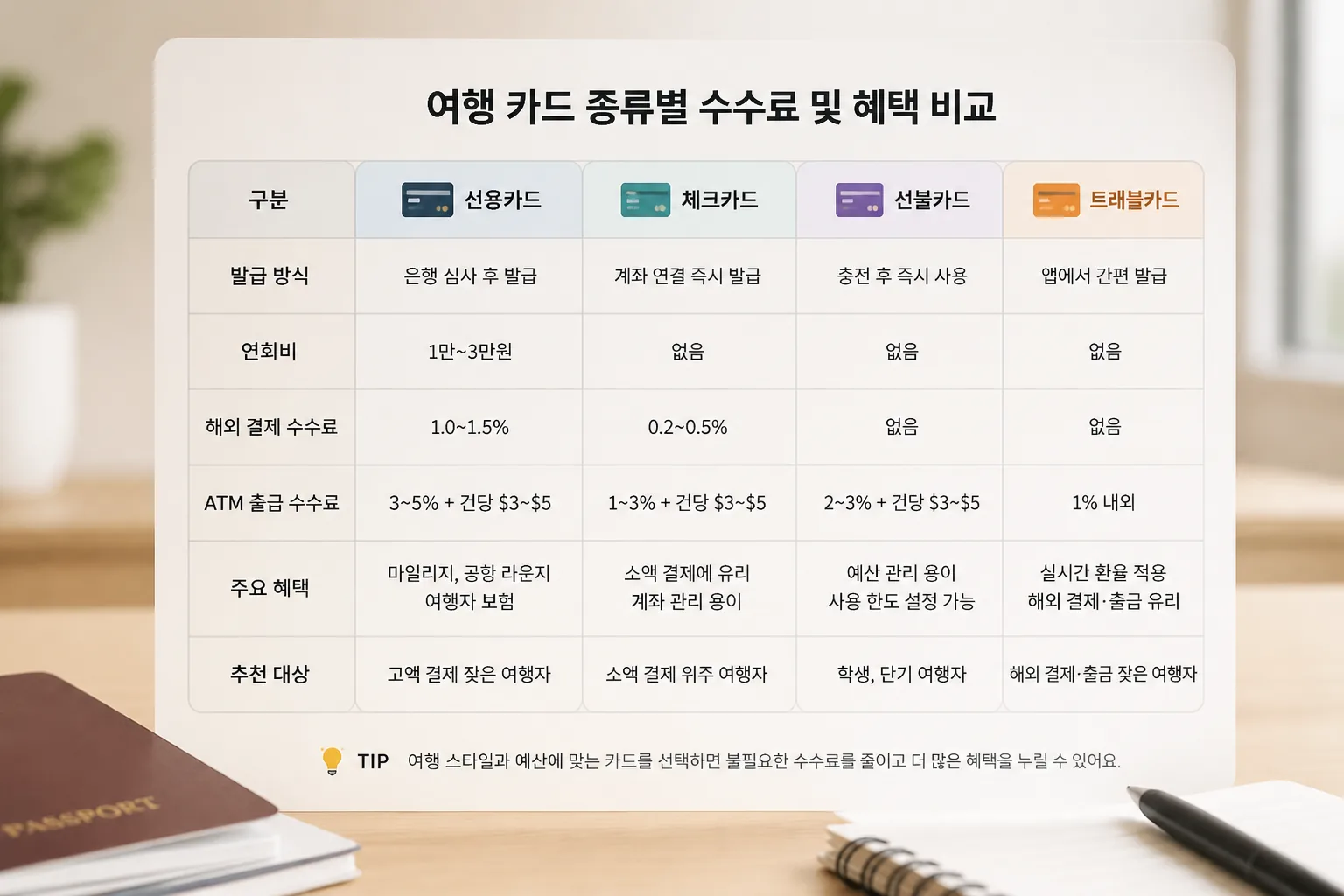

| Card Type | Annual Fee | Typical Bonus | Best Use | Main Catch |

|---|---|---|---|---|

| Flexible points | $95 | 50k-75k points | Flights and transfer partners | Higher spend requirement |

| Airline card | $0-$99 | 40k-70k miles | One airline loyalty | Less flexible redemption |

| Hotel card | $0-$99 | 80k-150k points | Weekend stays | Hotel points can be weak |

| No-fee travel card | $0 | 20k-30k points | Beginners with tight budgets | Lower upside |

| Cash-back card | $0 | $200-$300 | Simple trip savings | No transfer sweet spots |

01 A big bonus can pay for the flight. The wrong card can wreck June.

If you’re graduating in May 2026 and eyeing a Memorial Day trip, the signup bonus matters more than the glossy airport-lounge photos. A 60,000-point offer can cover a round-trip domestic ticket worth roughly $600 to $900, depending on the airline and redemption method. But a $95 annual fee, a $4,000 spend in 3 months, and a thin entry-level income can turn a “free trip” into a budget hangover fast.

I’ve watched this play out with two recent grads in my circle: one used a bonus for a Denver-to-San Diego trip and paid the statement in full; the other chased points, overspent by $700, and carried interest at more than 20% APR. That second story wipes out the travel value in a hurry.

read our guide to choosing the right credit card first

The best travel card for a new grad is not the flashiest one. It’s the one you can clear every month.

TL;DR: look for a bonus you can earn with rent, transit, groceries, and one summer booking you were already planning. Skip any card that forces fake spending. That’s where the smart picks start.

02 5 card types worth watching in May 2026

Banks usually push travel bonuses around late May, right before summer booking spikes. You’ll likely see five lanes: flexible-points cards, airline cards, hotel cards, no-fee travel cards, and plain cash-back cards dressed up as travel tools.

Here’s the quick comparison:

| Card type | Likely fee | Common bonus shape | Best for |

|---|---|---|---|

| Flexible points | $95 | 50k-75k points | Flights, transfer partners |

| Airline card | $0-$99 | 40k-70k miles | Loyal flyers |

| Hotel card | $0-$99 | 80k-150k points | 2-4 hotel nights |

| No-fee travel | $0 | 20k-30k points | Tight budgets |

| Cash back | $0 | $200-$300 | Simplicity |

My bias? For most grads, flexible points or cash back win. Airline and hotel cards shine only when you already know your summer route or property. A friend who moved to Atlanta last year got huge value from a Delta-style setup. Another grad heading through three cities did better with bank points she could move around. Same season, different answer. Next up, the spending rule is where the real math gets ugly.

03 What nobody tells you about the minimum spend

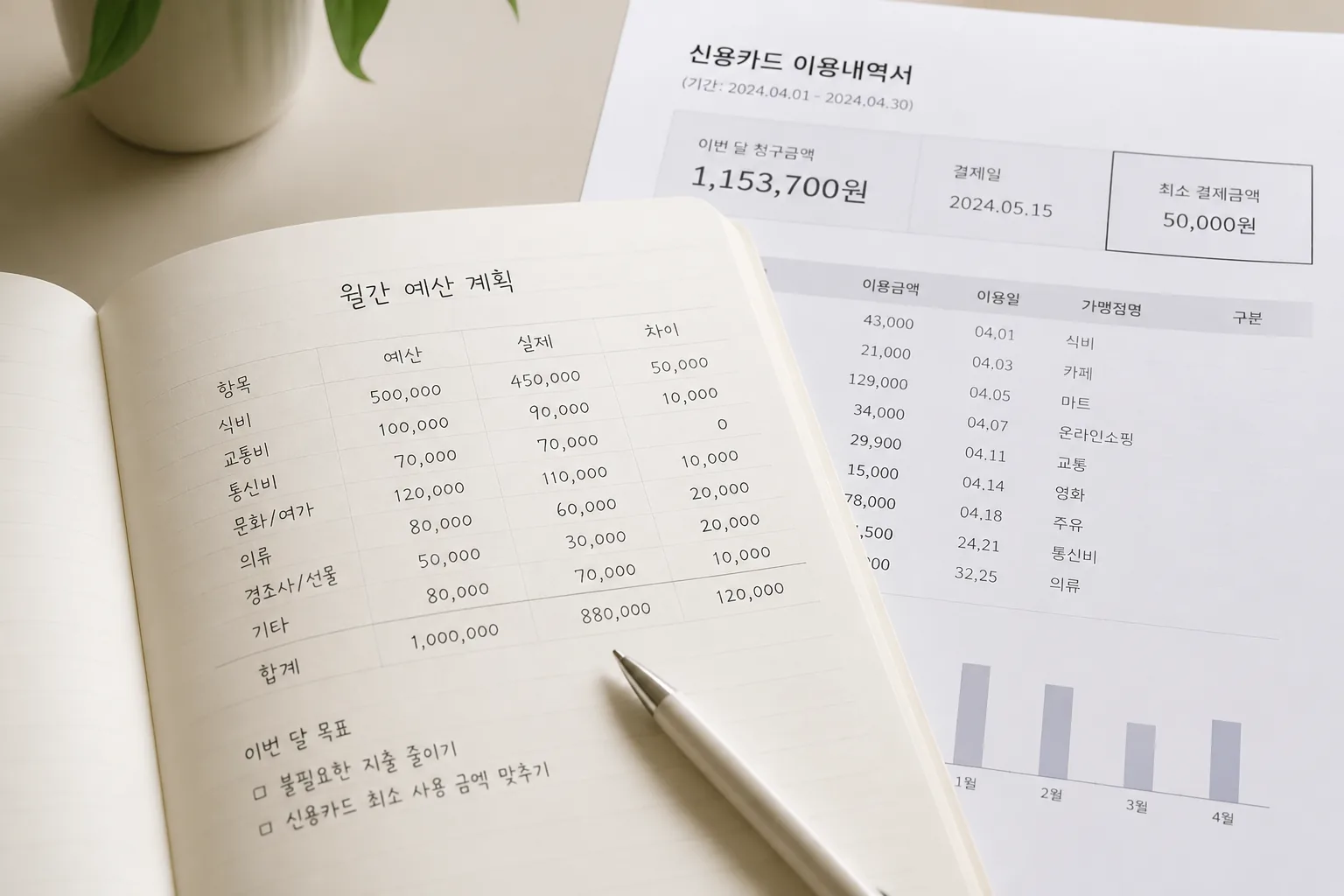

A 70,000-point bonus sounds amazing until the fine print says spend $4,000 in 90 days. For a new grad earning $48,000 a year, that could be nearly a full month of take-home pay. If your normal 3-month spend is closer to $1,800 or $2,400, the card is asking you to become a different person overnight. Bad idea.

The better play is boring, and boring works. Look for offers tied to $500, $1,000, or $2,000 thresholds if you’re just starting out. Pair that with statement autopay.

see our simple budget plan for first-job finances

A travel card should fund the trip after graduation, not delay your emergency fund until September.

That brings us to the part tucked into the keyword that actually makes this whole strategy safer.

04 The dividend cash flow angle, without the fantasy

That Korean phrase, 배당 cash flow strategy, points to a simple idea: use steady cash flow to support goals without stretching your paycheck. For a recent grad, that does not mean buying dividend stocks just to justify travel spending. Honestly, that’s backwards.

A smarter version looks like this:

- Build a 1-month cash buffer first.

- Put recurring bills on a card you can pay in full.

- Treat any dividend income, HYSA interest, or side-hustle cash as a trip offset, not permission to overspend.

If you already own a small dividend ETF and it throws off $20 to $30 a month, great. Use that to cover baggage fees, award taxes, or the annual fee. If you don’t, focus on income stability first. That’s the grown-up move, even if it’s less exciting than points screenshots on TikTok.

read our beginner guide to dividend investing

Quick recap:

- Best fit: flexible points or no-fee cash back

- Red flag: spending goals above your real 90-day budget

- Best use of side income: offset travel costs, don’t inflate them

One last thing matters before you apply: timing.

05 Before you apply this Memorial Day week

May 2026 bonuses could shift daily around Memorial Day weekend, so don’t lock in the first shiny offer you see at 11:47 p.m. Compare the public offer, the annual fee, transfer partners, and the first-year value after fees. Plain cash back can beat points if your trip is one short flight and two cheap hotel nights. That surprises people every year.

Do these 3 things today:

- Check your last 90 days of spending and write down the real number.

- Compare one flexible-points card, one no-fee card, and one cash-back card.

- Price your actual trip in dollars and points before applying.

If the math works before the application, the bonus feels like a gift. If not, it’s just marketing with better lighting.

Related:

see our guide to redeeming points without wasting value

The short version? A recent grad should chase fit, not hype. If the bonus covers part of a summer trip and the balance gets paid in full, great. If the card pushes you into debt for a beach photo, skip it. There will always be another offer next month.