If you’re already paying for groceries, gas, and bills every month, your card could be doing more. The right travel rewards setup might quietly cut the cost of your next trip.

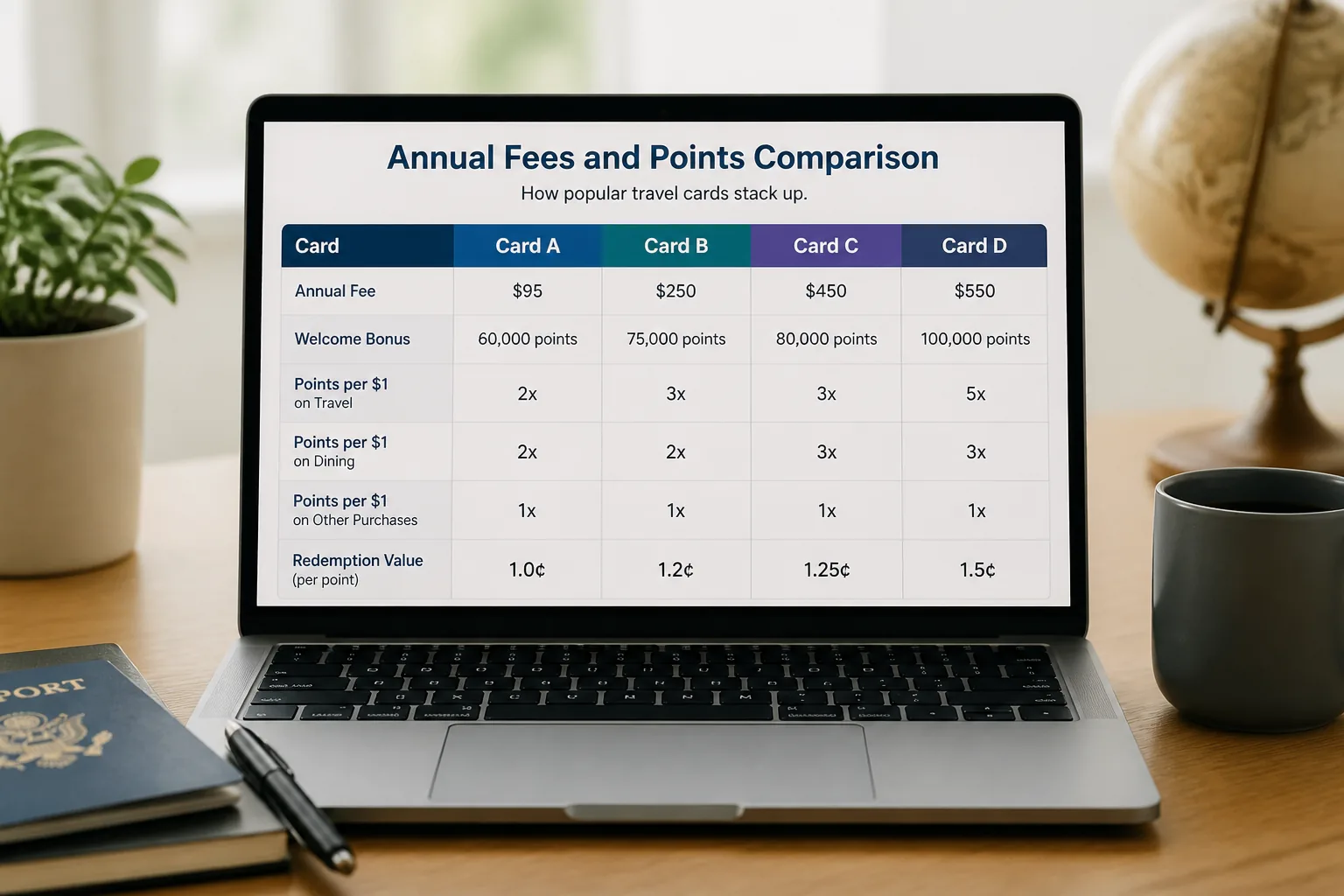

| Card Type | Annual Fee | Best For | Typical Rewards Angle | Key Perk |

|---|---|---|---|---|

| Flexible Points Card | $95-$395 | Most travelers | Transferable points | Strong redemption options |

| Airline Card | $0-$150 | Brand-loyal flyers | Miles on airline spend | Free checked bag |

| Hotel Card | $0-$199 | Frequent hotel guests | Hotel points | Anniversary free night |

| Flat-Rate Travel Card | $0-$95 | Simplicity seekers | Steady earning | Easy redemptions |

| Premium Travel Card | $395-$695 | Frequent travelers | High-value points plus credits | Lounge access |

01 Travel rewards credit card picks, minus the marketing fluff

Ever open a card comparison page and feel like every offer is “worth” $1,000? That’s usually where people start losing money.

A travel rewards credit card can be a smart tool, but only if the math works for your habits. A card with a $95 annual fee, 60,000-point bonus, and no foreign transaction fees may be great for a traveler flying 6 times a year. The same card can be a bad deal for someone taking one weekend trip to Miami in October. I’ve watched friends chase shiny signup bonuses, then carry a balance at 24% APR. That wipes out the reward fast.

This guide compares 5 common card types by annual fee, rewards rate, transfer value, and travel perks. You’ll also see where lounge access matters, where it really doesn’t, and how to avoid paying for benefits you’ll never touch.

See our guide on comparing credit cards side by side

sets up the broader basics if you want the full framework first.

The best travel card is rarely the flashiest one. It’s the one that matches your actual spending.

02 The 5 card types worth your attention

Here’s the short list most readers actually need.

- Flexible points card — usually $95 to $395 annual fee, points transfer to airline and hotel partners, strong for people who want options.

- Airline card — often $0 to $150 fee, best for loyal flyers chasing free checked bags or priority boarding.

- Hotel card — annual fee often pays back through a free night certificate, though only if you redeem it.

- Flat-rate travel card — simple earning like 2x on travel or 2% back toward trips, less drama, fewer sweet spots.

- Premium luxury card — $395 to $695 fees, airport lounge access, statement credits, and better trip protections.

What matters here is redemption value. Bank points can land around 1 cent each in a portal, sometimes 1.25 to 1.5 cents on better redemptions, and 2 cents or more with strong transfer partner bookings. But that higher value takes work. Think of it like buying a great chef’s knife. Amazing tool, sure, but only if you actually cook.

03 Where the big bonus helps, and where it bites back

A 60,000-point bonus can cover a domestic round-trip ticket, sometimes more. Sounds great, right? But the spending requirement is the trap door.

Say a card asks for $4,000 in 3 months. If you already spend $1,400 a month on rent, groceries, gas, and insurance, fine. If you force that spend with impulse purchases, the bonus gets expensive fast. A friend of mine did exactly that in 2024 with a premium airline card, then paid interest for 5 months. Brutal.

Pros that matter:

- Big early value from bonuses

- No foreign transaction fees on many travel cards

- Travel protections like trip delay or rental coverage

Cons people underestimate:

- High annual fees after year one

- Points devaluations by airlines or hotels

- Credits that sound easy but go unused

Credits feel like savings. Sometimes they’re just pre-paid spending.

Next up, let’s narrow this down by traveler type, because that’s where the best choice gets obvious.

04 Match the card to the trip, not the ad

If you travel once or twice a year, a mid-fee flexible points card usually wins. You get decent rewards, transfer options, and protections without paying luxury-card prices.

If you fly Delta, United, or American 8 to 12 times a year, an airline card can save real cash through checked bag fees alone. One round-trip bag can cost $35 each way on domestic routes. Four trips a year for two people? That’s $560. Suddenly a $99 annual fee looks pretty reasonable.

Quick recap:

- Occasional traveler: keep fees low, value simplicity

- Brand-loyal flyer: chase airline perks, not just miles

- Hotel regular: look hard at anniversary night value

- Frequent traveler: premium perks can pencil out

For a deeper money strategy around fees and rewards,

Read more about smart everyday money habits

is a useful companion.

The last piece is simple, and honestly, it’s the part most people skip.

05 Three moves to make before you apply

Start with your last 90 days of spending. Pull up your banking app and total dining, groceries, flights, hotels, and gas. That number tells the truth.

Then check three things:

- Annual fee after year one

- Foreign transaction fee, ideally 0%

- Redemption path: cash back, portal, or transfer partner

Oh, and one more thing. Look at your credit score before any application spree. Two hard pulls in 30 days may be fine for some people, but stacking 4 or 5 cards for bonuses gets messy fast.

Related: credit score habits that protect approval odds

can help if you’re close to the edge.

Good rewards come from planned spending, not extra spending.

If you want the safest default, pick a card with a modest fee, flexible points, and no foreign transaction fee. If you travel constantly, premium perks may earn their keep. Either way, make the card fit your life, not the other way around. Period.