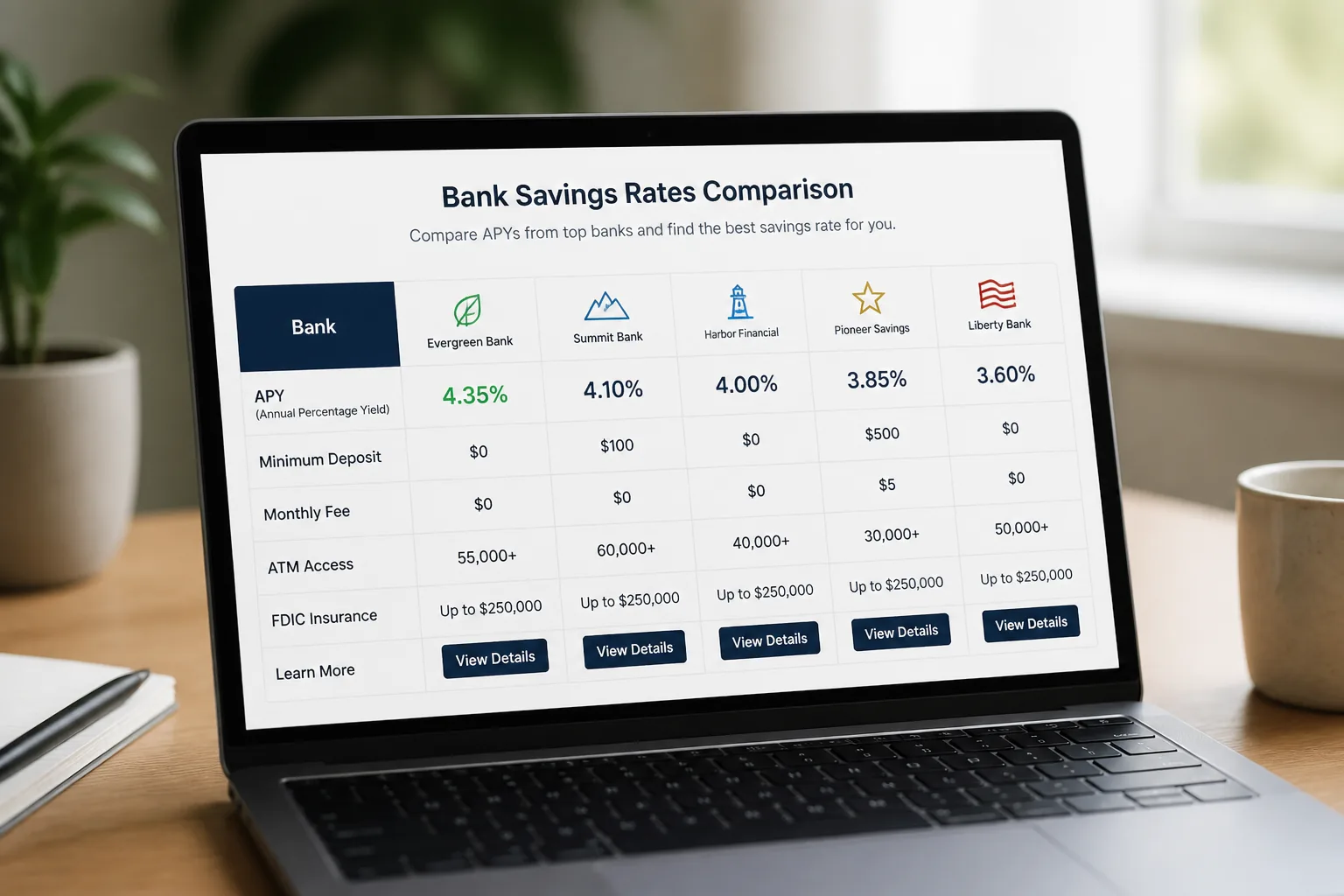

If your savings balance hasn’t moved much, the account itself may be the problem. A quick rate comparison can change the math fast.

| Account | Typical APY Position | Monthly Fee | Standout Feature | Best For |

|---|---|---|---|---|

| Marcus by Goldman Sachs | Usually competitive | $0 | Simple interface | Straightforward savers |

| Ally Bank | Usually competitive | $0 | Savings buckets | Goal-based saving |

| Discover Online Savings | Mid-to-high range | $0 | Recognizable brand | Balanced convenience |

| Capital One 360 Performance Savings | Competitive | $0 | Pairs well with checking | Existing Capital One users |

| American Express High Yield Savings | Competitive | $0 | Trusted brand familiarity | Brand-conscious savers |

| Synchrony High Yield Savings | Competitive | $0 | Access-focused options | People who value flexibility |

| SoFi Savings | Can be very strong | $0 | Rate may depend on setup | Users comfortable with account requirements |

01 High Yield Savings Account Comparison: start with the 4 numbers that matter

Ever move your savings for an extra 0.50% APY, then realize transfers take 3 business days? That little detail can matter more than the headline rate.

Here’s the short version: a smart high yield savings account comparison comes down to APY, fees, minimum balance, and access speed. Online banks usually beat big brick-and-mortar names by a wide margin, but the highest advertised rate is not always the best fit for your emergency fund. I’ve watched friends chase a flashy promo, then get annoyed by app glitches or slow external transfers. That’s the trade-off nobody mentions in the ad copy.

If you’re weighing savings options,

read our guide to investment basics for beginners

pairs well with this decision because cash reserves and investing should work together, not compete.

The best account is the one that pays well and lets you sleep at night.

Quick comparison snapshot:

| Account type | Typical APY range in 2025 | Monthly fee | Best for |

|---|---|---|---|

| Online HYSA | 4.00%–5.00% | $0 | Emergency funds |

| Credit union savings | 3.00%–4.50% | $0–$5 | Local service |

| Big bank savings | 0.01%–1.00% | $0–$15 | Existing relationship |

The gap looks small until you run the math, and that’s where this gets interesting.

02 7 picks for 2025, broken down like a real-world shortlist

You don’t need 27 tabs open. You need a clean shortlist.

1. Marcus by Goldman Sachs — strong reputation, no monthly fee, usually competitive APY. Good for savers who want a simple dashboard.

2. Ally Bank — solid app, no monthly fees, buckets feature for goal-based saving. Great for people who like organizing money visually.

3. Discover Online Savings — easy interface, no fee, known brand. A comfortable middle ground.

4. Capital One 360 Performance Savings — easy to pair with checking, useful if you want one login.

5. American Express High Yield Savings — recognizable name, often competitive APY, straightforward setup.

6. Synchrony High Yield Savings — decent rate history and ATM card access on some savings products, which some savers like.

7. SoFi Savings — attractive rates can depend on direct deposit or account setup, so read the terms twice.

No single pick wins for every person. The real question is why one account feels effortless while another becomes a headache by week two.

03 What nobody tells you about access, limits, and the fine print

A savings account earns interest, sure. But it also needs to behave well in real life.

Three details deserve a hard look:

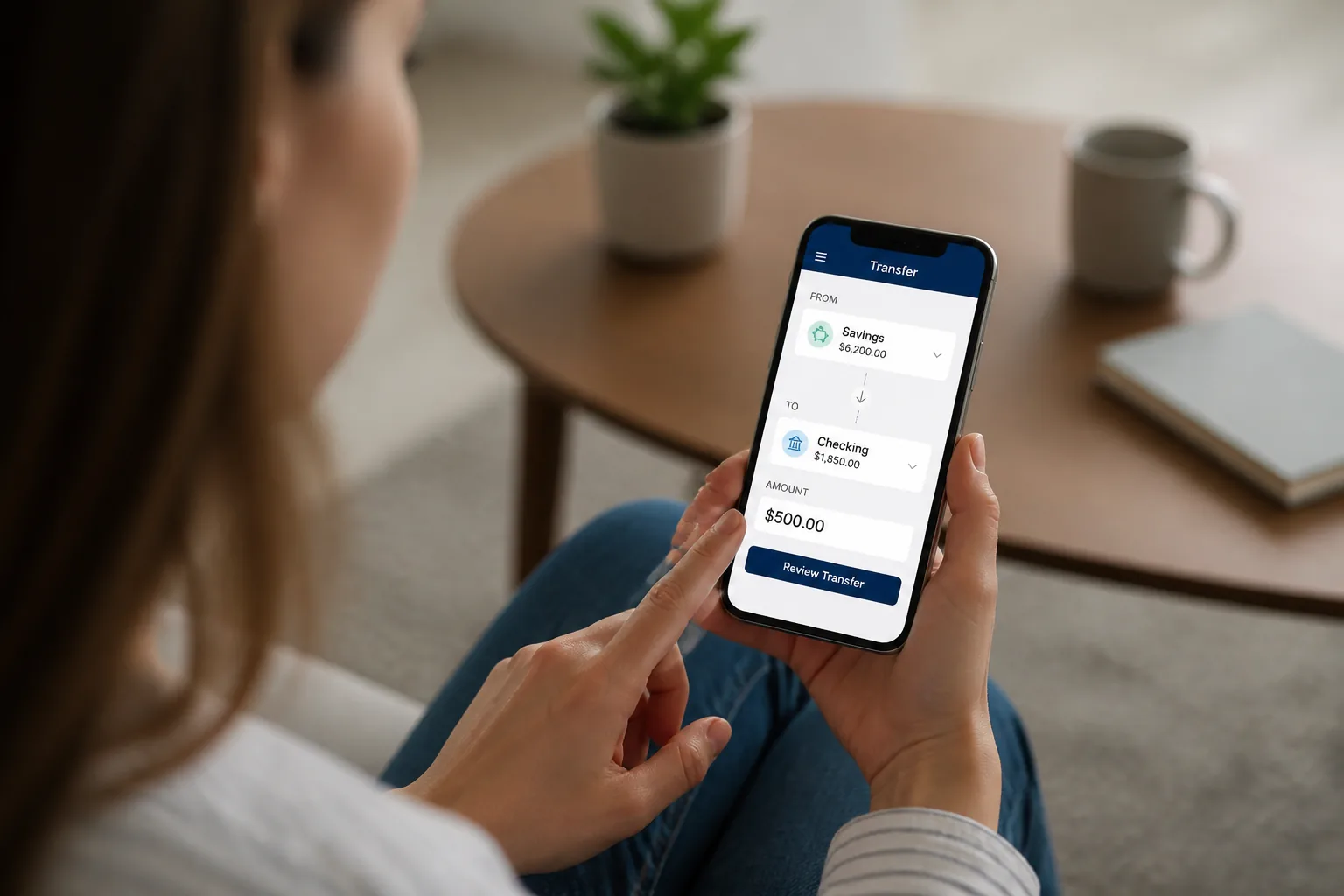

- Transfer speed: Some banks move money in 1 business day, others take 2 to 3.

- Minimums: Many online accounts have $0 minimums, but a few reserve the best experience for larger balances.

- Support quality: Chat at 11 p.m. sounds great until you need a human on a Friday afternoon.

A cousin of mine kept her emergency fund at a big national bank earning under 1.00% APY because she liked the branch on Main Street. Fair enough. Then she compared that with an online account near 4.50% APY on $15,000. That’s roughly

. Honestly, that surprised her.

Chasing the top APY while ignoring access is like buying the cheapest flight with a 14-hour layover.

Next up, let’s match account styles to actual savings goals, because emergency cash and a vacation fund should not be treated the same way.

04 Which account fits your goal? That’s the part people skip

This is where the comparison gets useful.

If you’re building an emergency fund, favor reliability over the absolute top rate. Ally, Marcus, Discover, and Capital One 360 often appeal to people who want a clean app and predictable transfers. If you’re saving for a 6-month goal like a car repair buffer or wedding deposit, a slightly fussier account with a stronger APY may be worth it.

For savers who already bank with one institution, convenience has value. Period. Logging into one dashboard can keep you consistent, and consistency beats rate-hopping for most households. Still, if your current bank pays 0.10% and an online option pays 4.50%, loyalty gets expensive fast.

related: credit card comparison for everyday spending

see our guide on budgeting methods that actually stick

Quick recap:

- Pick APY from a reputable, FDIC- or NCUA-insured institution.

- Check fees and transfer timing before opening.

- Match the account to the job the money needs to do.

That final step is where good choices turn into smart ones.

05 My practical take: compare less, decide faster

A high-yield savings account should make your cash work harder without making your life harder. That’s the standard.

Here’s my honest take after reviewing the field: online savings accounts usually win on yield, while established brands and all-in-one banks win on comfort and convenience. Neither camp is wrong. You just need the one that matches your habits.

Do these 3 things today:

- Check your current savings APY and write down the exact number.

- Compare 3 accounts on APY, fee, minimum, and transfer speed.

- Move a test deposit first, then shift the full balance once you trust the setup.

A better savings account won’t change your finances overnight, but over 12 months, the gap gets real.

If your cash is sitting in a low-rate account, this is a fix you can make in under 20 minutes. That’s a pretty good return for one small decision.