Trying to choose between an index fund and an ETF? They can look almost identical at first, but the small differences can shape your returns and your routine.

| Fund Type | Typical Cost | Trading Style | Best For |

|---|---|---|---|

| Index Mutual Fund | 0.03%-0.10% | End-of-day pricing | Automatic monthly investing |

| ETF | 0.03%-0.10% plus spread | Real-time market trading | Taxable accounts and flexibility |

01 The short version before you buy anything

Ever stare at index fund vs ETF and think, “Aren’t these basically the same thing?” You’re not wrong. A Vanguard S&P 500 index mutual fund and an S&P 500 ETF can own near-identical stocks, yet the way you buy, automate, and pay taxes on them feels very different by Friday afternoon.

When I first compared the two, the surprise wasn’t performance. It was friction. One fit autopilot investing like a 401(k). The other felt more like using a brokerage app with extra control. If you’re building long-term wealth, that small difference can shape years of behavior.

read more about investment basics for beginners

Same ingredients, different packaging. That changes how real people invest.

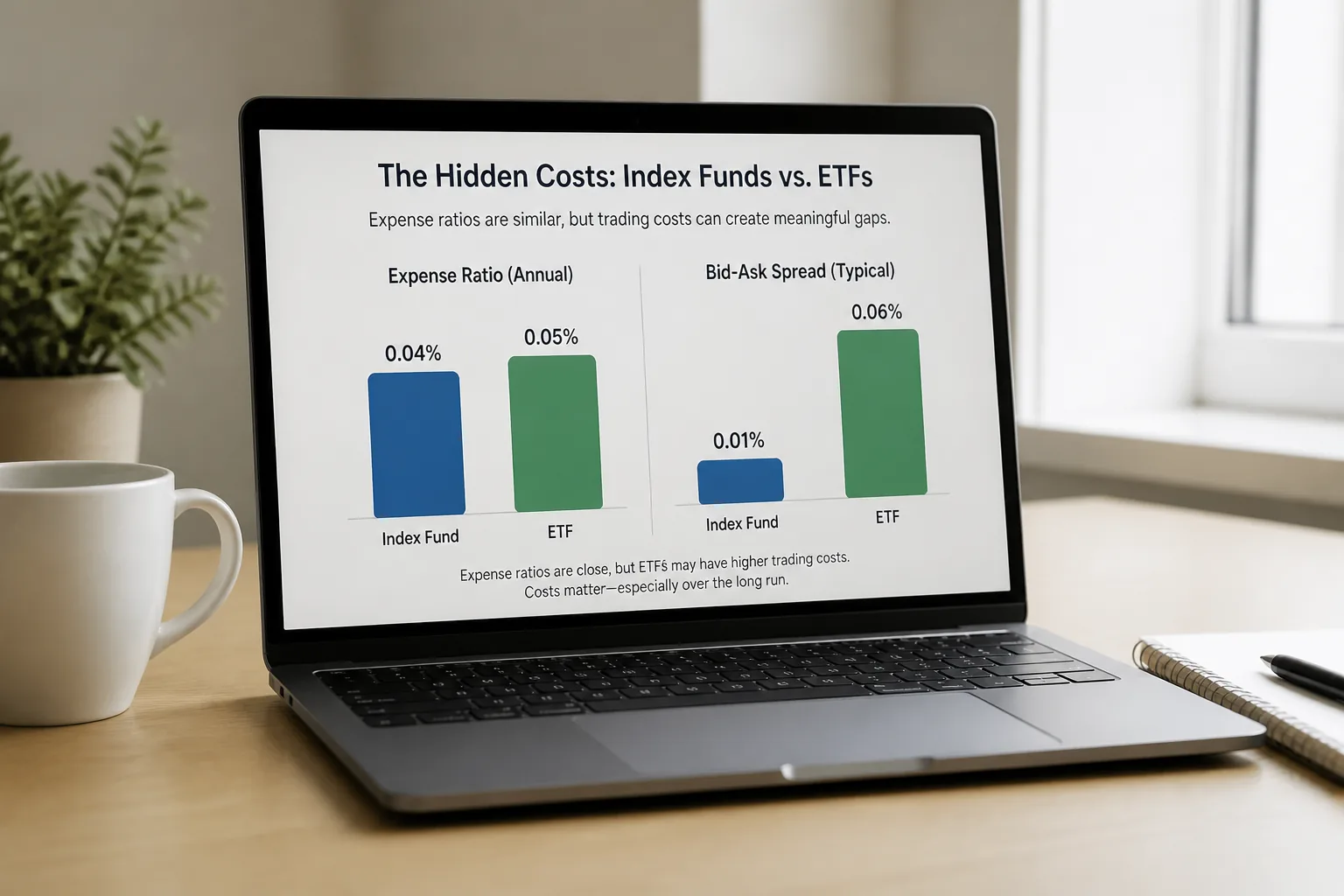

02 5 cost gaps that actually matter

Start with expense ratios, but don’t stop there. Many broad-market funds now charge tiny fees: 0.03%, 0.04%, sometimes 0.05%. On a $10,000 balance, that’s roughly $3 to $5 a year. Pretty small.

But here’s the thing: the hidden costs can matter more. ETFs may have bid-ask spreads, especially in thinly traded funds. Mutual-fund index funds can carry minimums like $1,000 or $3,000 at some firms, though many brokers now waive them.

A quick side-by-side helps:

| Feature | Index Fund | ETF | Why it matters |

|---|---|---|---|

| Trading | End-of-day NAV | Real-time market price | Control vs simplicity |

| Minimum | Sometimes $1 to $3,000 | Usually price of 1 share | Easier entry for small accounts |

| Spreads | None | Small trading spread | Adds cost on each trade |

| Automation | Usually easy | Broker-dependent | Huge for monthly investing |

03 Where the real divide shows up: taxes and trading

This is where ETFs often pull ahead in taxable accounts. Because of the in-kind creation and redemption process, ETFs have historically been more tax-efficient than many mutual funds. That’s why investors with large brokerage balances often lean ETF.

A friend of mine in Chicago kept a plain S&P 500 fund in a taxable account for 6 years and barely touched it. Fine choice. Another used ETFs because he harvested losses in 2022 when the market dropped hard. Same market exposure, better flexibility. That’s a real difference.

Index funds win on behavioral simplicity. You buy at the close, ignore the noon drama, and move on with your life. ETFs tempt some people to check prices at 10:17 a.m., 1:42 p.m., and right before dinner. Sound familiar?

If real-time pricing makes you trade more, the feature becomes a bug.

04 Who should pick what? Keep it brutally practical

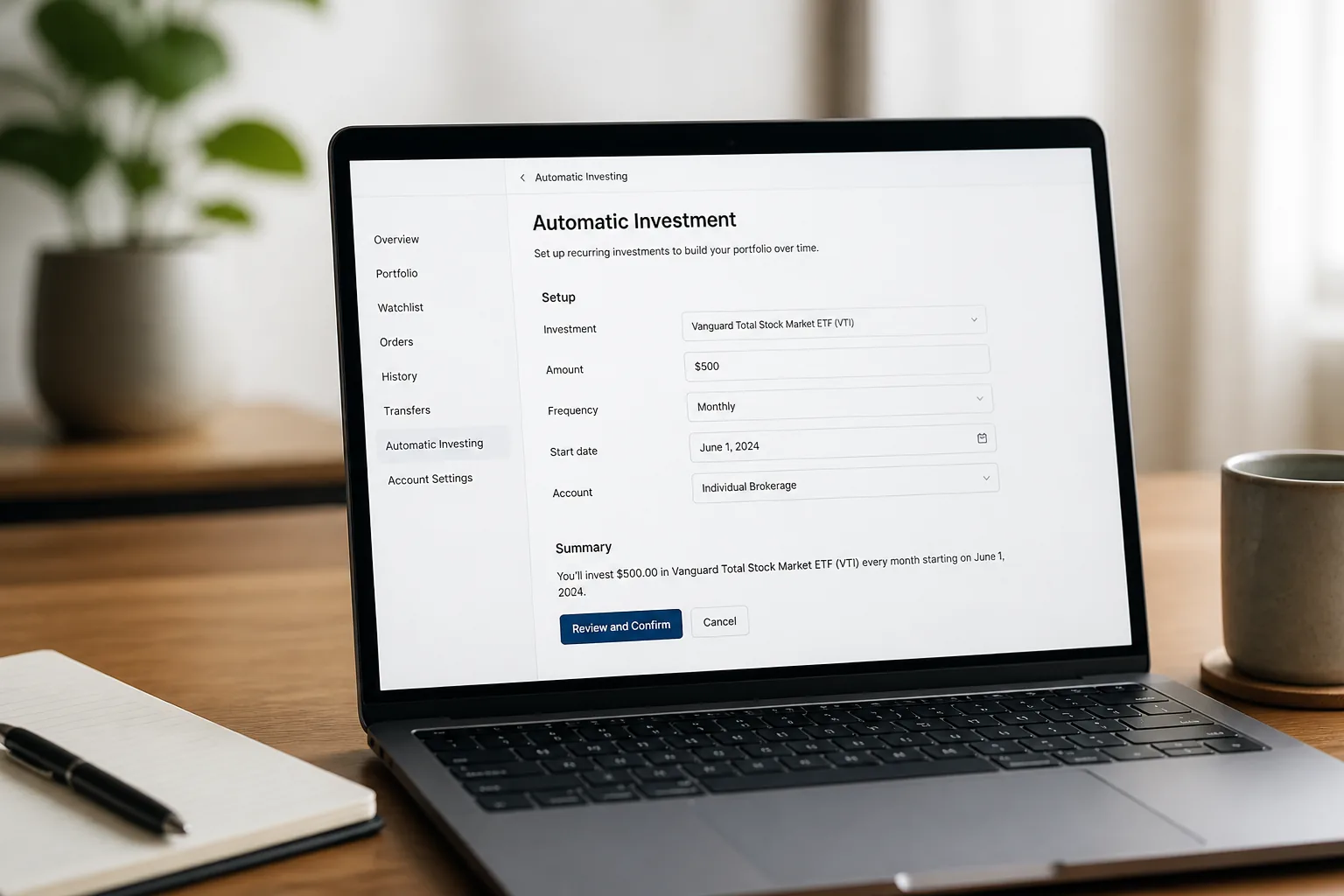

If you’re investing $300 every month from a paycheck, an index mutual fund often feels cleaner. Automatic contributions, automatic purchases, no need to think about share prices. That matters at month 3 and even more at year 7.

If you’re using a taxable brokerage account, want intraday control, or buy through a platform that supports fractional ETF shares, ETFs can be the better fit. Charles Schwab, Fidelity, and Robinhood all made this easier over the past few years. Honestly, that’s why ETFs exploded with younger investors.

Quick recap:

- Choose index funds for hands-off automation and disciplined saving

- Choose ETFs for tax efficiency, portability, and lower entry barriers

- Choose either if the fund tracks the same benchmark and you can hold it for 10+ years

see our guide on Roth IRA basics

05 What to do today, before you overthink this

You do not need the perfect wrapper. You need a setup you’ll stick with through boring months and ugly ones. That’s the part people skip.

- Open your brokerage today and check whether recurring ETF purchases are available.

- Compare the expense ratio, minimum investment, and average spread on one broad-market fund.

- Decide where the money sits: taxable account or retirement account. That answer narrows the choice fast.

If you want the cleanest rule, here it is: pick index funds for automation, ETFs for flexibility. Then keep contributing. That’s usually the winning move.

related article: simple portfolio rebalancing rules